BRIEFLY NOTED: FOR 2021-11-03 We

Things that went whizzing by I want to remember:

First:

Jason Zweig soft peddles the idiocy of Kevin Hassett and James Glassman on the 18 years-late Dow 36000 day. Buy-and-hold is a good investment strategy for the U.S. stock market. The strategy Hassett and Glassman were pushing—borrow money, leverage up, and go highly long stocks near the peak of a valuation-ratio bubble—led to bankruptcy in 2000 for anyone who acted on the recommendations of Dow 36000. Jason here is much kinder than I would have been:

Jason Zweig: Dow Crosses 36000—Making a Book’s Prediction Just Two Decades Late: ‘This week, the book “Dow 36,000” by James Glassman and Kevin Hassett turned out to be prophetic. The Dow Jones Industrial Average should hit that mark “very quickly,” “immediately,” even “today,” the book had proclaimed. “The rational time frame is this afternoon,” wrote Messrs. Glassman and Hassett, although they conceded it might take “three to five years.” The book was published Oct. 1, 1999, when the Dow closed at 10273. More than 22 years later, the index very briefly crossed the mark at 9:42 a.m. on Monday, in a moment barely noticed by investors. The book’s prediction finally came true…. On Jan. 17, 2012, with the Dow at 12482 and used copies of “Dow 36,000” selling around that time for as little as one penny, a reviewer using the pseudonym “Annyong Bluth,” a character from the television comedy “Arrested Development,” gave the book a five-star review on Amazon.com. It wasn’t what most people would consider positive, though. “I used the pages of this book to line the base of our two-month-old Rottweiler puppy’s cage,” the reviewer wrote. “I was struck by the moisture and odor-absorbing power of its pages. These super-absorbent sheets really took to canine urine and feces. And, at 1 penny for 294 pages, Dow 36,000 was such a steal! Highly recommended!”… As for “Dow 36,000,” after years of insisting that the book’s thesis was correct, Mr. Glassman finally wrote in an opinion piece in the Journal in February 2011: “I was wrong.” Saying the world had become “a riskier place” since 1999, Mr. Glassman urged investors to scale back their stock holdings. The Dow closed at 12068.50 that day. Since then, the Dow has tripled…

LINK: <https://www.wsj.com/articles/dow-jones-36000-stock-market-predictions-glassman-hassett-11634823650>

What is Kevin Hassett saying today, on Dow 36,000 day? In my inbox:

In a wide-ranging interview with _Washington Post Live_ today, author Kevin Hassett discussed his warning that high inflation will drive the U.S. economy into a recession and his new book, The Drift: Stopping America’s Slide Toward Socialism. Hassett is a former senior adviser and chair of the Council of Economic Advisers under President Donald Trump…. ‘The fact is that socialism doesn’t work’: “The fact is that socialism doesn’t work. And when you pursue strategies other than profit maximization, then you don’t maximize productivity, you don’t maximize wages… Even the Scandinavians when they move to the U.S., their standard of living skyrockets.” Hassett says income inequality ‘dropped sharply’ while President Trump was in office: “Donald Trump comes in and pursues very capitalist policies… and those policies had a massive positive effect on ‘social justice.’ You know, the number of people living in poverty dropped by six million… Income inequality skyrocketed before President Trump came to office, and dropped sharply when he was in office.” Hassett on how to help the middle class: “I think the best way to help the middle class is the way we did it during the Trump administration which is to encourage businesses to expand, to cut corporate taxes so that there’s a big increase in capital formation, that increases productivity, that drives wages up…

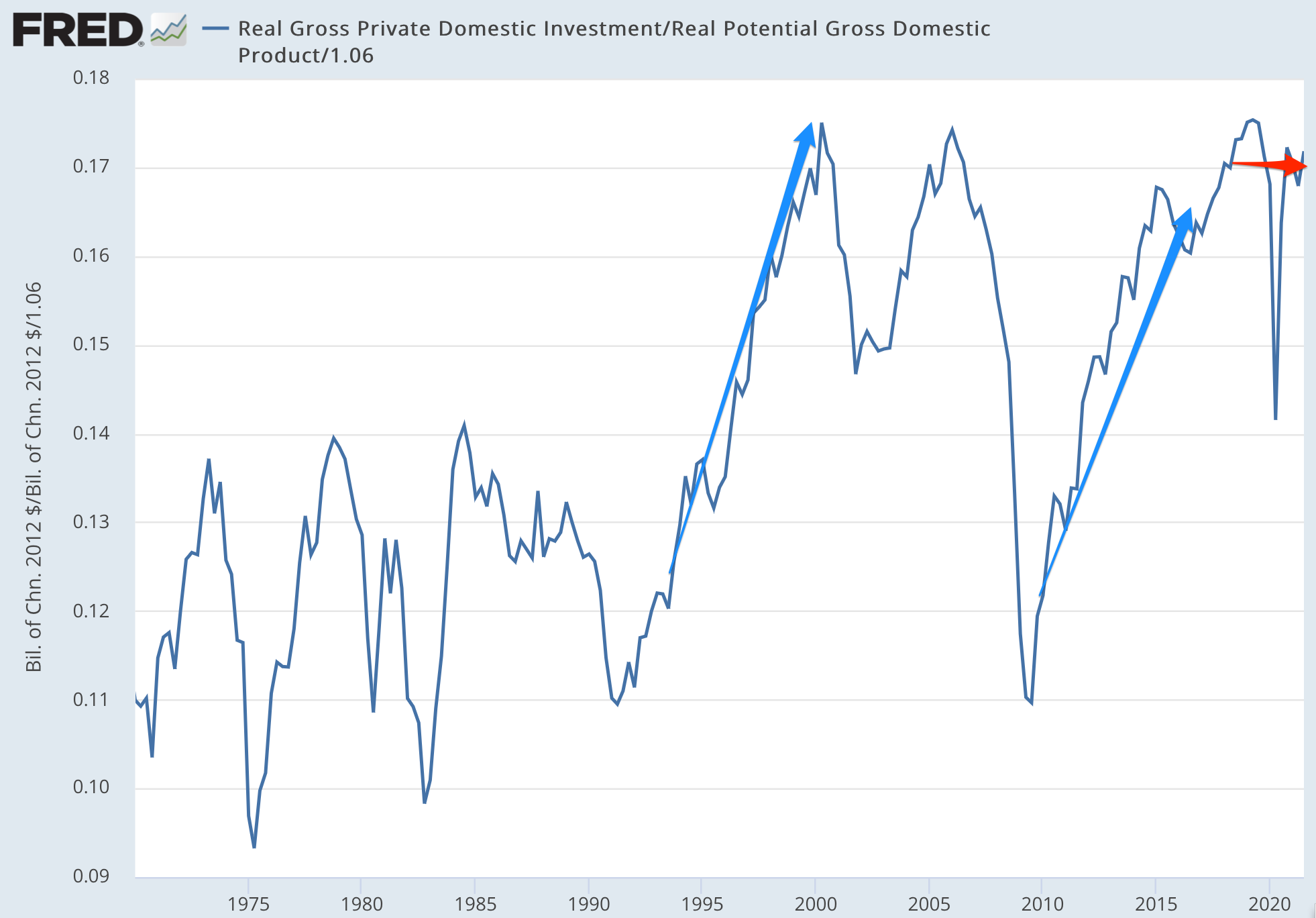

Hassett knows that there was no big increase in capital formation after the Trump-Ryan-McConnell corporate income tax cut he helped design. The big increases in capital formation came (a) under Clinton due to smart policies, and (b) under Obama as the economy recovered from the Great Recession that grew out of policies and circumstances that took place on George W. Bush’s watch. The red arrow shows the effect on capital formation of Trump-Ryan-McConnell: none. Hassett knows that. But his Washington Post Live interviewers didn’t know and didn’t care to learn:

It is, admittedly, an accomplishment to give corporations as large a tax cut as the one Hassett helped design without managing to give them incentives to increase capital formation. But Hassett did it. Republicans who worked for Trump—or for George W. Bush, or for George H.W. Bush, or for Ronald Reagan—should not boast about how their policies will or did increase investment in America. They should not boast at all.

One Video:

Pat Gelsinger: Intel CEO Q&A Roundtablee <https://www.youtube.com/watch?v=N_j2yI7xzCc&t=25s>:

Very Briefly Noted:

Jason Furman & Wilson Powell III: Worker Bargaining Power Has Been No Match For High Inflation: ‘Real compensation growth has been below trend in all sectors apart from leisure and hospitality… <https://www.piie.com/blogs/realtime-economic-issues-watch/worker-bargaining-power-has-been-no-match-high-inflation>

Gideon Rachman: The Moment of Truth Over Taiwan Is Getting Closer: ‘The US and China are engaged in a dangerous game of military poker over the future of the island… <https://www.ft.com/content/9833d499-07ce-40eb-84e7-436023c6eb8b>

Rajiv Sethi: Notes on a Remarkable Finding from Finlandn: ‘the understanding of meritocracy in public discourse is terribly impoverished. If one wTre to design a truly meritocratic policy, it could well have features that resemble the pursuit of representation targets. Meritocratic policies will not, in general, involve the application of a common score threshold across all candidates…

Paragraphs:

Michael Pettis: China’s Economy Needs Institutional Reform Rather Than Additional Capital Deepening: ‘Consider European countries after 1918 or Europe and Japan after 1945… highly advanced economies that had been devastated by war and thrown into poverty, but because their institutions remained largely intact, they were nonetheless able to grow extremely quickly…. They had… very high Hirschman levels…. But after many years of spectacular growth driven by capital deepening (in large part restoring the infrastructure and manufacturing capacity that had been wrecked by war), each of these countries reached that point again, after which their growth rates slowed rapidly. Their actual levels of investment had “caught up” not to the capital frontier set by the United States but rather to the Hirschman levels consistent with their own domestic institutions. The same has been true of China. When the reform era began in the late 1970s, the country had emerged from five decades of anti-Japanese war, civil war, and Maoism that had left it terribly underinvested—relative not to the capital frontier set by the United States, but rather, more meaningfully, to a Hirschman level of investment that its own institutions allowed it to absorb productively…. In China’s case, the fastest way to develop in the 1980s and 1990s was to increase capital deepening as rapidly as possible. But… it was always just a matter of time before it reached its own Hirschman level…. Being further behind economically does not increase the probability of catch-up except in specific cases, usually in cases where, for historical reasons (like war, revolution, political circumstances, or incompetence), a country’s level of investment has fallen far behind its Hirschman level, which is itself determined by the development level of the country’s institutions. The so-called middle income trap is, in my opinion, a recognition of this fact…. What China really needs is a transformation of its institutions in a direction that some might argue is very different from the direction it is currently following…

LINK: <https://carnegieendowment.org/chinafinancialmarkets/82362>

Don Kalb: HAU Not: For David Graeber & the Anthropological Precariate: ‘I told my students that O[pen ]A[ccess] in academia might perhaps be a possibility, but… more likely… endless exploitation of precarious academics on every level. And that it would serve to fortify the prestige economies of the old Ivy League–Oxbridge axis…. It was an unsustainable proposition to run a journal without money, unless you could trade on old prestige and turn that into the fictitious accumulation of a pyramid scheme for a few year…

Enrique Martino: The Bullshit Hit Job: David Graeber & the Hau “Coup”: ‘Analytical summary of 93 pages of email correspondence between David Graeber, Ilana Gershon, Sarah Green, one postdoc and one graduate student, in addition to messages from Marshall Sahlins, Marilyn Strathern, Sean Dowdy and members of the anthropology departments of SOAS and Stanford, from November 11 to December 25, 2017, regarding Giovanni da Col and HAU…

Gregori Galofré-Vilà & al.: Austerity & the Rise of the Nazi Party: ‘Areas more affected by austerity (spending cuts and tax increases) had relatively higher vote shares for the Nazi Party…. Localities with relatively high austerity experienced relatively high suffering…. Our findings are robust to a range of specifications including an instrumental variable strategy and a border-pair policy discontinuity design…

Alberto Alesina & al.: ‘On the Origins of Gender Roles: Women and the Plough: ’Traditional agricultural practices influenced the historical gender division of labor and the evolution and persistence of gender norms…. Descendants of societies that traditionally practiced plough agriculture, today have lower rates of female participation in the workplace, in politics, and in entrepreneurial activities, as well as a greater prevalence of attitudes favoring gender inequality. We identify… by exploiting variation in the historical geo-climatic suitability of the environment for growing crops that differentially benefited from the adoption of the plough…. To isolate the importance of cultural transmission as a mechanism, we examine female labor force participation of second-generation immigrants living within the US…

LINK: <https://scholar.harvard.edu/files/alesina/files/ontheoriginsofgenderroleswomenandtheplough.pdf>

Gillian Brunet: Stimulus on the Home Front: The State-Level Effects of WWII Spending: ‘I use newly-digitized contract data on U.S. war production spending…. I estimate a local fiscal multiplier of 0.25, implying an aggregate multiplier of roughly 0.25 to 0.3. Employment effects are commensurately small…. Two features of the wartime economy significantly reduced the stimulative effect of wartime spending. Conversion from civilian manufacturing to war production reduced the direct shock to economic activity because war production directly displaced civilian manufacturing. Saving and taxes account for 75% of the income generated by war spending, implying that the add-on effects from increased consumption were minimal…

LINK: <https://berkeley.app.box.com/v/JMP-Brunet-current>

Ha ha, that Schaede & Mankki paper is great!

The basic point, that *conditioned on test score*, a group with less test preparation will on average have a higher inherent ability than a group with more preparation is obvious enough. But the genius is in finding a situation where imposing a minimum quota on *males* improves results! That's bound to wind up the "meritocracy".

I wasn't as impressed by Sethi's claims for monotonicity, unconnected as they are to any empirical support; in that context, the "extremely likely" assertion has a contrary effect. I think it plausible that training is weakly observable (in the sense of a group average) but his model rests on the assumption that it is strongly observable (for each individual) and he ought to provide some empirical support for this assumption even if he can't find any for his conclusion. But whatever, that is a secondary question IMO.