DeLongTODAY: GameStonk 2021-01-29

Just what happened with respect to the GameStop short squeeze? And how can you have a public short squeeze if there is no fundamental news that makes people uncertain & fear that the shorts might b...

…e wrong?

From <http://.delongtoday.com>

On Tuesday, January 26, 2021, Tesla CEO Elon Musk tweeted out one word—GameStonk!!—with two exclamation points, and with a link to a board on the internet discussion site Reddit, a board that describes itself as: “WallStreetBets: Like 4chan found a Bloomberg terminal”. The word “GameStonk” is a mashup of “stonk”, a misspelling of “stock”, and “GameStop”—the Dallas-headquartered U.S. bricks-and-mortar videogame retailer with 5000 stores, $1 million of annual revenue per store, and currently $200 million a year of losses. The misspelling of “stock” means that Musk wants his readers to know that he is adopting a pose of enthusiasm and excitement: the pose is that he must communicate, and cannot be bothered to spellcheck anything before he sends his words out to the internet. “GameStonk!!” could therefore be translated thus: “excitement, enthusiasm, and approval for (or perhaps for what is currently going on with) the stock of the company GameStop.”

The price of GameStop (ticker $GME) immediately rose 60%.

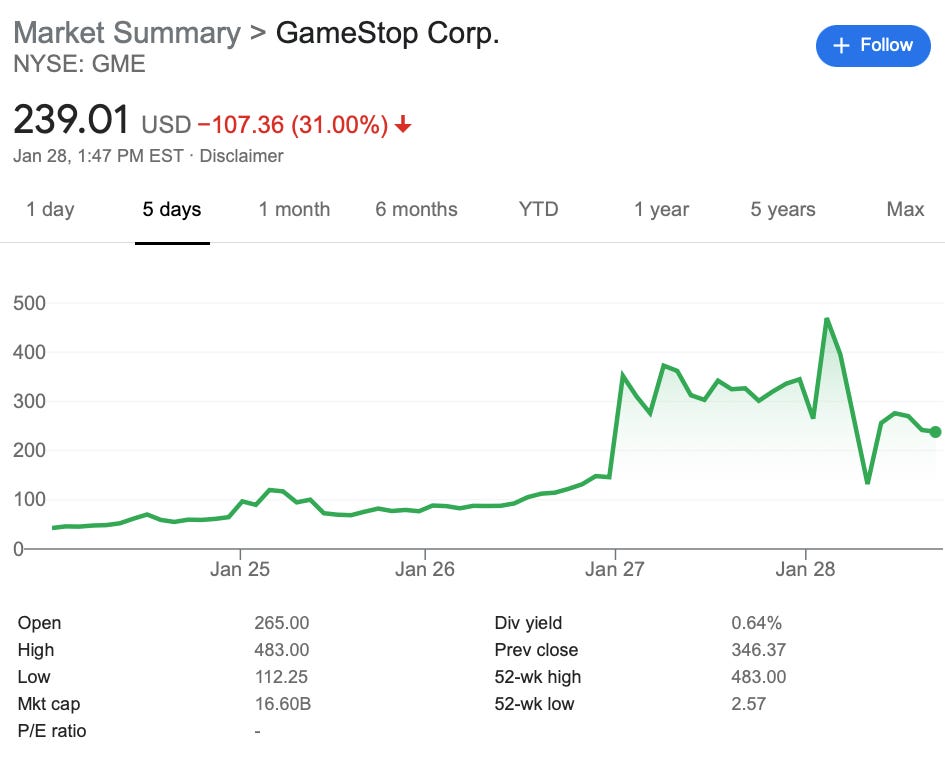

The stock had doubled earlier in the day. The supposed trigger was early Facebook executive and current venture capitalist Chamath Palihapitiya’s tweeting that he had bought call options on GameStop, betting the stock would go still higher than it had before. The total equity value of GameStop was $5.5 billion Tuesday morning, $11 billion Tuesday afternoon, $17 billion Tuesday evening, a peak (so far) of $26 billion Wednesday, and $18 billion Thursday as I am taping this.

OK. So what is going on? And what does this mean?

Wikipedia tells us that GameStop is headquartered in suburban Dallas, TX, near to a LEGOLAND:

GameStop is an American video game, consumer electronics, and gaming merchandise retailer. The company is headquartered in Grapevine, Texas, United States, a suburb of Dallas, and operates 5,509 retail stores throughout the United States, Canada, Australia, New Zealand, and Europe as of February 1, 2020. The company's retail stores primarily operate under the GameStop, EB Games, ThinkGeek, and Micromania-Zing brands. In addition to retail stores, GameStop also owns Game Informer, a video game magazine.

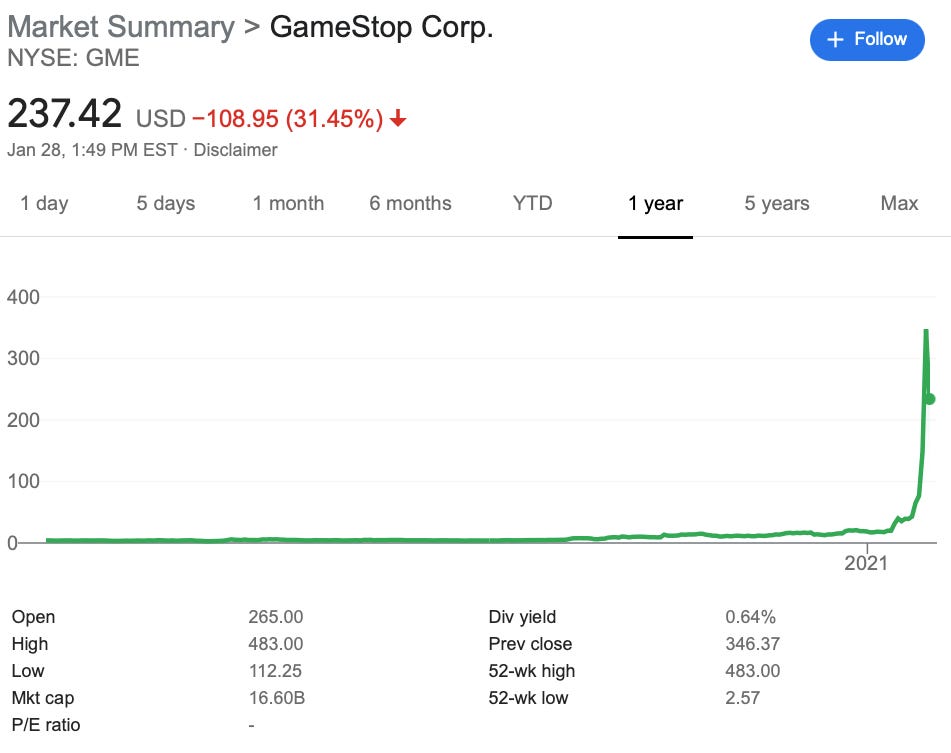

GameStop last made a profit in calendar 2017: $35 million. It lost $673 million in 2018, lost 20% of its revenue in 2019 down to $6.46 billion for a loss of $471 million, looks to realize $5.26 billion in revenue and lose $200 million, and is forecast—but tracking analysts forecasts are usually optimistic—at revenues of $5.84 billion and break-even in 2022. Up until September, it was worth some $5 per share, $350 million for the 70 million shares outstanding.

The stock jumped in September and October—roughly tripled, boosting the company’s equity valuation from about $350 million to about $1 billion. Why? Because of Ryan Cohen. Ryan Cohen had founded online pet retailer MrChewy in 2011 at the age of 25. He had made a success of it, selling it to PetSmart for $3.35 billion and stepping down from the CEO position in 2019. He had bought 10% of GameStop. He hoped to turn it around: “GameStop needs to evolve into a technology company that delights gamers and delivers exceptional digital experiences—not remain a video game retailer that overprioritizes its brick-and-mortar footprint and stumbles around the online ecosystem…” he wrote.

Before Ryan Cohen’s appearance, the consensus was that GameStop would be closed in a decade. The market’s valuation was that of the $50 billion in revenue the firm might collect before it closed, it would be generous to think that 1% of that might be ultimately paid out to shareholders. Afterwards, the market was more optimistic: maybe with Ryan Cohen involved, there was a 20% chance GameStop could, instead, become an internet property as valuable as MrChewy was when Cohen sold it to PetSmart. Maybe Ms. Market was right here; maybe Ms. Market was wrong. I tend to think that Ms. Market was being too enthusiastic about the ability of one charismatic 35er with successful experience in an adjacent market segment to make a big difference. But I would not say that I was at all sure that Ms. Market was wrong.

One other thing happened in September-October: an extra 35 million shares or so were shorted. As of August, there were 100 million shares in long positions—people who stood to gain if GameStop went up or paid dividends—and 30 million shares in short positions—people who stood to gain if GameStop went down. By the end of October there were 135 million shares in long positions in 65 million shares in short positions. And then nothing happens until January 12, 2021.

So what happens in the two weeks between the end of January 12 and dawn on January 26? The stock-market valuation of the company then went from $1 to $5.5 billion. Why and how?

One part of it is a “technical” story. The technical story has two parts. The first part is the “short squeeze” part. Suppose that you are a short seller. And suppose that the price of a stock you have shorted goes up—goes way up. What do you do? On the one hand, the profits from your short, if it comes in, are now much bigger, so you hold on to and may well increase your short position.

On the other hand you are now poorer—perhaps a lot poorer—and your tolerance for risk goes down. Moreover, you are in this as a business: you cannot get yourself into a situation where one bet going wrong will destroy your ability to make other bets in the future, no matter how big a winner this one bet looks. And, in addition, the fact that the stock has moved against you is evidence that your initial analysis of the situation was, to some degree at least, not accurate. Those will tend to make you shrink your position.

The net effect of these factors is that, for short sellers, their demand curve may well slope the wrong way. Markets are stable because when price goes up demand tends to go down. But if short-sellers decide to cover rather than increase their positions when the price rises, their component of the demand curve does not slope down but slopes up—unless and until much bigger short sellers with much deeper pockets and much greater risk tolerances are attracted into the market.

The second part of the technical story is the call option part. Suppose you want to bet on Ryan Cohen’s success—or bet that it might look like he might possibly be a success. You could buy the stock. Or you could amplify your potential winnings by buying a way-out-of-the-money call option on the stock. That way you can make a bet that might come in really big, and make it cheaply. If you think you have more knowledge than capital, and yet you want to limit your downside exposure by not borrowing to buy stock and hence being on the hook if the stock goes bankrupt, a call option can look attractive.

The question is: who do you buy the call option from? If you can find somebody who wants to make the opposite bet—to bet that Ryan Cohen will not succeed—well and good. But odds are you will buy the call option from somebody who does not have strong views about Ryan Cohen and GameStop. They simply want to collect some money for making a market up front, and then be out of the game. They do not want to gamble. They want to hedge their position.

How do they hedge their position? Well, they sell you a call option and then they buy a little bit of the stock at the market price. If the call option price goes up, it must be because the stock price has gone up. When the call option is way out-of-the-money, a $1 increase in the stock price produces only a very small increase in the value of the option, so you do not need to buy much stock. But as the stock price approaches the option strike price—the price at which you get to buy the stock if you “call” your option—the proper delta hedge requires more and more of the stock. And at the limit, as the option comes into the money, the delta hedge amount becomes one.

Thus as the stock price goes up, your counterparty who has sold you the option must increase his or her long position in the stock in order to stay hedged. From your perspective, you are not doing anything as the stock price rises. You have an option. You are just letting it ride as the stock bounces around. But the combination of you-and-your-counterparty-who-has-hedged-their-position as a unit is another positive-feedback trader: somebody else whose demand curve slopes the wrong way, with your collective demand for the stock not falling but rising as the stock price rises.

And, of course, as the stock price rises, it gains more mindshare. And some of those whom news about the stock touches will decide to buy.

So far we have three factors: short-sellers who can be squeezed, and thus turned into positive-feedback traders; counterparties of call option purchasers, who are positive-feedback traders as well; and the fact that news and buzz is a source of stock demand. There are also three more factors: call them YOLO (as Matt Levine does), rage-against-the-(financial)-machine (as John Authers does), and pump-and-dump.

Let me quote from Matt Levine on YOLO:

The people on the WallStreetBets subreddit sometimes all get into a stock at once. This is fun, a nice social outing in an age of social distancing, a risky but potentially lucrative collective entertainment. Recently they decided to do GameStop. Because, I don’t know, they’re gamers… it’s a little comical to pump the stock of… mall video-game stores during a pandemic, or because… professional investors are short GameStop and they thought it’d be funny to mess with them. Or, especially, because their friends on Reddit were buying…. Take one person who’s long for fundamental reasons, add 100 people who are long for personal-amusement reasons like “lol gaming” or “let’s mess with the shorts,” and then add thousands more who are long because they see everyone else long, and the stock moves: “‘It was a meme stock that really blew up’, said WallStreetBets moderator Bawse1…. GameStop seemed so utterly doomed that the current situation was actually sort of funny to the subreddit’s denizens. Banded together, WallStreetBets members bought in big enough to move the stock…. Here is a seven-hour YouTube video from Friday in which a guy called “Roaring Kitty” dips a chicken tender in champagne to celebrate his GameStop wins. “This is the thing, overbought can stay overbought, remain overbought, even get more overbought,” he says, which is as good a summary of the situation as anything else…

And let me quote from John Authers on rage-against-the-(financial)-machine:

I argued that it was misplaced to take pleasure at the pain for the short-sellers who had attacked GameStop stock, and then been subjected to a “short squeeze” for the ages by traders coordinating on Reddit. I received a bumper crop of feedback… leaving out many with unprintable expletives): “How much did [GameStop short-position hedge fund] Melvin pay you to write this garbage? shill. Literally trying to protect an industry trying to fleece jobs from low income workers. Sleep well chump…” “Watching entitled institutional shorts whine… that millennials equipped with margin accounts & zero fees are collaborating on Reddit to target them is my new favorite sport. Looks perfectly healthy… plus 1 for the little guys.” “Normal isn't putting the retail trader down for being independent while organized hedge funds force you to take their way or suffer in fear. Normal is the American dream and being able to make your own way. This isn't a casino. This is a riot…”

We coordinated our purchases on Reddit, and we got rich, and in the process we made a bunch of overrich institutional Wall Street plutocrats sad and poorer. What is not to like?—that seems to be their view.

Well, what is not to like is that ultimately all the money there is is the dividends that will be paid by GameStop and the price that will be paid by its acquirer whenever the GameStop corporate shell is dissolved and its assets are repositioned. At the moment those who have sold GameStop on its ride up have collected perhaps $14 billion—$7 billion from the shorts and $7 billion from current GameStop holders who were late into their long positions. The short-sellers have lost $7 billion. Current stockholders of GameStop have an asset

worth $14 billion that they paid $7 billion for—and so a paper profit of $7 billion right now. But the only value to back GameStop is the money that will be flowing out of the firm as distributed profits—and that is likely to be $400 million only, or maybe $700 million, or maybe $1 billion at best.

Current GameStop shareholders are thus looking to lose at least $6 billion of the $7 billion they have paid for the stock—unless they find greater fools willing to take their shares off their hands at something like its current $14 billion paper-profit valuation.

And here we get to the pump-and-dump question: How much do those who have already received $14 billion in profits from GameStonk so far overlap with those who currently hold a $14 billion paper position in GameStonk—a position that was $28 billion at one moment Thursday afternoon? And how much have those who have profited already dumped their positions? And what role did those who have profited play in pumping up the stock in the first place?

Combine pump-and-dump, rage-against-the-(financial)-machine, YOLO, hedged call options as strong sources of positive-feedback trading, and the short squeeze with the excitement provoked by the hope that Ryan Cohen could repeat his success with MrChewy, and you have the stage set for Elon Musk and Chamath Palihapitiya to trigger the quintupling of Tuesday and Wednesday. It is hard to know why they did what they did. It seems likely to be YOLO—for if they had positions, they are likely to spend the rest of their lives enmeshed in nets of lawsuits.

The story is really reminiscent of the bad old days of Gilded Age Wall Street—the Harlem corner, the stats bearcat corner, the Northern Securities panic. (The family story is that one of my great-great grandfathers killed himself with his revolver because he could not face telling his family the scale of his losses in Northern Securities).

There is, however one big difference. In previous search episodes of short squeezes, corners, and massive immediate fast-moving bubble divergences of market prices from fundamentals, there was considerable uncertainty about what those fundamentals really were. Was the stock being pumped above its value by cynics who wanted to dump it later? Or were people who had learned that there was about to be great news about the business trying to quietly buy it up in advance? And were the rumors that there was a pump-and-dump going on false-flag diversions to keep the general public from getting in on a good thing?

Before there was always a universe to be understood and mastered, or Masters of the Universe who you could profit be emulating. Knowledge either about what fundamental values really were or about the plans of insiders. But this time there is no knowledge, there is no pattern.

Just as Donald Trump was a reality-TV simulacrum of a president, so this feels like a reality-TV version of financial Robber Barons. A going-through-the-motions for the camera, but, somehow, not the real thing. Then there was a reason to think things might work out as planned.

Now there is only: GameStonk!!

I keep wondering why it is that the short sellers here are not like the London Whale, in that people found out what you were up to, and decided to use it to their financial advantage. Now just who wins when this all shakes out is an open question, of course.