Looking at: Diane Coyle: "Cogs & Monsters"

& BRIEFLY NOTED: For 2021-12-14 Tu

First:

How should economists be changing what they do?

Diane Coyle: Cogs & Monsters: ‘This book reflects my frustration with the straw men arguments [against economists]…. They have allowed economists to overlook or deny some things that are badly wrong with the discipline….

The extent to which economics—specifically financial economics in this case—actually shapes the world rather than just analysing it.

How hard it is to analyse the society you are part of, looking particularly at macroeconomics….

The need for economists, especially those working in policy roles, to take more account of the way their own actions change the economy… by shaping a climate of ideas that affects norms of behaviour.

Acceptance that… while we should always aim to be impartial and evidence-based, economists are themselves powerful, and yet often unaccountable, political actors….

Finally, the need to assemble the building blocks available in much existing economic research into a benchmark framework appropriate to the digital economy, and to provide suitable policy tools reflecting the framework.

It will be apparent that I do not think that this [last] shift is much in evidence, even though there are indeed building blocks available, particularly in sub-fields such as industrial organisation and market design, information economics, or growth theory. However, although the blocks are there, they have not been assembled into a consistent structure and above all do not address the welfare economics questions. Nor are there the kinds of models, tools, and rules of thumb needed to translate these insights into the classroom and the offices of policy analysts….

I am convinced that a changed ‘mainstream’ paradigm is needed and will emerge. The reason? Events. Digital technologies…. Globalisation… technologies…. The dual hit of the 2008 financial crisis and the 2020 coronavirus crisis…. It is surprising that so little changed in the way the global economy has operated after the shock of 2008–2009. It may well turn out that, like a cartoon character that continues running for a while beyond the edge of the cliff, the consequences were yet to come. The two shocks combined cannot fail to have a lasting effect, just as the Depression and the Second World War did almost a century ago…

LINK: <https://www.google.com/books/edition/Cogs_and_Monsters/zjUoEAAAQBAJ>

I find myself not so sure and not so optimistic as Diane: it took World War I, a failure to restore gold-standard stability and growth in the following decade, the Great Depression, and World War II—all four of them—to knock the world out of the pseudo-classical (because it was, in fact, not old but quite new) semi-liberal (because a great many people were deprived of their freedom, and a great deal of social power went not to the lucky and the entrepreneurial who were rewarded by the market but remained in the hands of semi-hereditary elites) order that it had been in before World War I.

All four were shocks that together prepared the soil for the post-WWII Age of Social Democracy that would follow, for the Thirty Glorious Years. Those were four big shocks—bigger than the ones we have had.

And then that Age of Social Democracy proved unsustainable: a relatively small (by our standards) productivity slowdown, a relatively small (by our standards) episode of high unemployment, and a decade of non-hyperinflation knocked the world economy knocked us from the Age of Social Democracy into the Age of Neoliberalism.

“The market giveth; the market taketh away: blessed be the name of the market” as an ideological formation buttressing semi-hereditary and status-based elites in the name of economic efficiency has proven to be a very strong factor in world history indeed. Keynes argued against it in the mid-1920s:

John Maynard Keynes: The End of Laissez-Faire: ‘Many elements have contributed to the current intellectual bias…. To suggest social action for the public good to the City of London is like discussing the Origin of Species with a bishop sixty years ago…. The lethargic monster… has ruled over us rather by hereditary right than by personal merit…. Let us clear…. It is not true that individuals possess a prescriptive 'natural liberty' in their economic activities. There is no 'compact' conferring perpetual rights on those who Have or on those who Acquire. The world is not so governed from above that private and social interest always coincide. It is not so managed here below that in practice they coincide. It is not a correct deduction from the principles of economics that enlightened self-interest always operates in the public interest. Nor is it true that self-interest generally is enlightened; more often individuals acting separately to promote their own ends are too ignorant or too weak to attain even these. Experience does not show that individuals, when they make up a social unit, are always less clear-sighted than when they act separately…

Thus I am markedly less optimistic than is Diane, not about economics—the state of economics, at least where I sit here in Berkeley, is very, very good. And we are, retirement by retirement, and RCT by RCT, gradually winning over economics to our view of how things are. It remains true that we do not yet have, as Diane laments, “a benchmark framework appropriate to the digital economy, and… suitable policy tools reflecting the framework…”, but that behavioral framework for the attention economy will come. For example:

But I am markedly less optimistic about discourse about the economy outside of the academy. Again, John Maynard Keynes back in 1926:

From the time of John Stuart Mill, economists of authority have been in strong reaction…. [J.M.] Cairnes, in the introductory lecture… in 1870…. “The maxim of laissez-faire… has no scientific basis whatever, but is at best a mere handy rule of practice.”… This, for fifty years past [i.e., since 1876], has been the view of all leading economists…. Nevertheless, the guarded and undogmatic attitude of the best economists has not prevailed against the general opinion that an individualistic laissez-faire is both what they ought to teach and what in fact they do teach…

“Laissez-faire is… what [economists] ought to teach, and what in fact they do teach.” A great deal of money rides on the successful propagation of that doctrine, and those who stand to benefit from its propagation have a great deal of money and so a great deal of social power. Thus as an economist it is very hard for me to believe that the doctrine will not continue to propagate.

Forthcoming September 6, 2022, from Basic Books:

Slouching Towards Utopia: A History of the Long Twentieth Century: Paragraph 7: Things changed starting around 1870. Then we got the institutions for organization and research and the technologies—we got full globalization, the industrial research laboratory, and the modern corporation. These were the keys. These unlocked the gate that had previously kept humanity in dire poverty. The problem of making humanity rich could now be posed to the market economy, because it now had a solution. On the other side of the gate, the trail to utopia came into view. And everything else good should have followed from that.

One Video

The Gesualdo Six: Veni, Veni Emmanuel <https://www.youtube.com/watch?v=MSRocN1dTrM>:

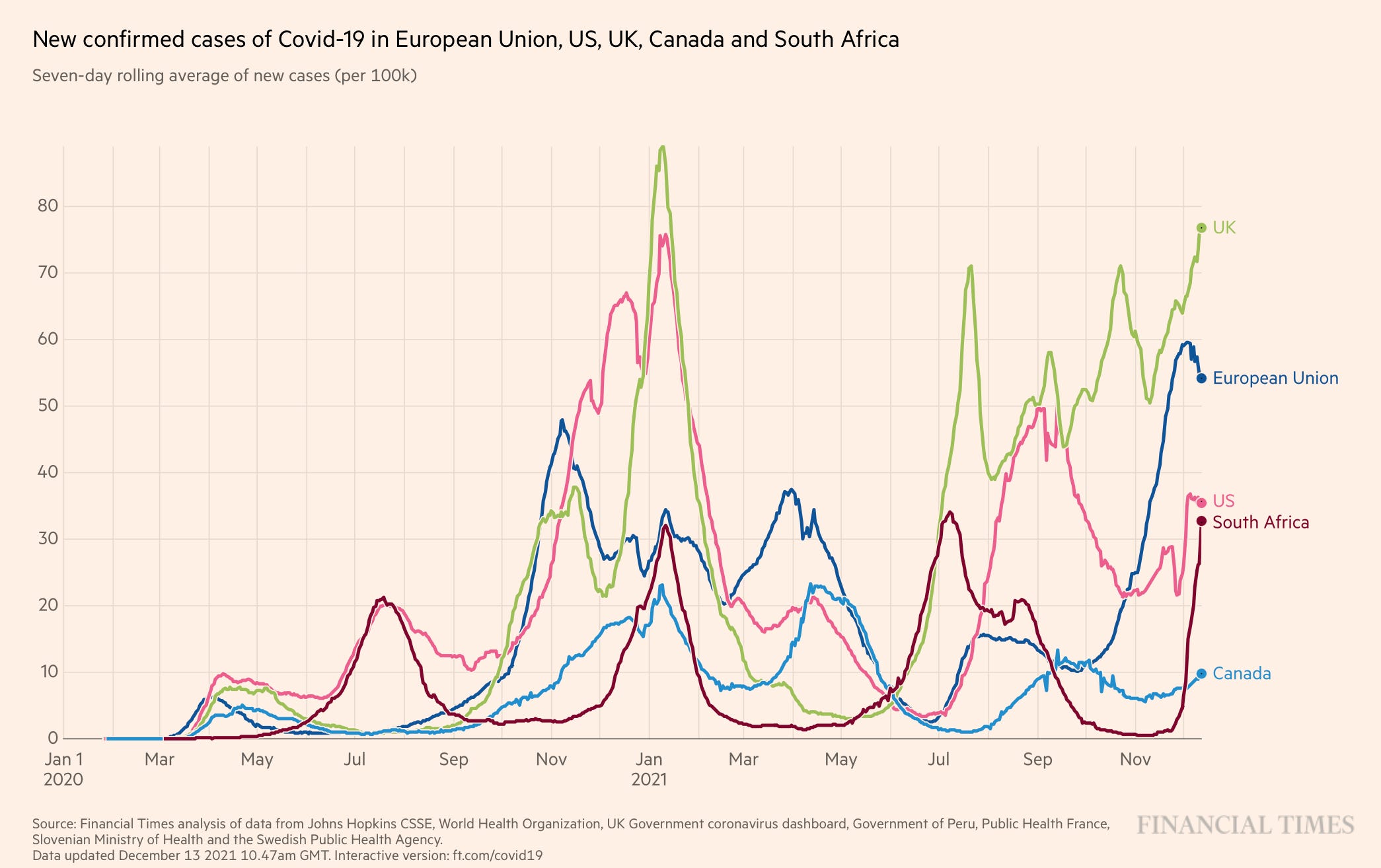

One Picture:

Very Briefly Noted:

Karmela Padavic-Callaghan: To See Proteins Change in a Quadrillionth of a Second, Use AI <https://arstechnica.com/science/2021/12/to-see-proteins-change-in-a-quadrillionth-of-a-second-use-ai/>

Jonathan Bernstein: Devin Nunes’s Retirement Says a Lot About Congress: ‘Powerful positions in the House aren’t what they used to be, especially on the Republican side…<https://www.bloomberg.com/opinion/articles/2021-12-13/devin-nunes-s-retirement-says-a-lot-about-congress>

Ben Thompson: Intel vs. TSMC, How Samsung and TSMC Won, MAD Chips: ‘The number one reason… is… Samsung and TSMC took huge risks and made huge investments at times and into business models that their competitors would not… <https://stratechery.com/2021/intel-vs-tsmc-how-samsung-and-tsmc-won-mad-chips/>

A Clerk of Oxford: The Anglo-Saxon O Antiphons <https://aclerkofoxford.blogspot.com/2013/12/the-anglo-saxon-o-antiphons-o-emmanuel.html>

Matt Levine: ’My list of books everyone in the financial industry should read would be Liar’s Poker, Barbarians at the Gate, Diary of a Very Bad Year and this complaint <https://t.co/64ljmQbzY5>… <

Paragraphs:

Eric Topol: Omicron Is Getting More Defined: ‘With Omicron, based on a limited number of UK cases, the 2-dose protection dropped down to 34, and boosted up to 75%. That is a big decline from Delta… potentially associated with about a 5-fold higher breakthrough infection rate after a booster…. The rapid growth of Omicron is especially alarming, with a doubling rate between 2–3 days in multiple countries…. We have the mitigation tools to defend against its transmission but have not been using them. California just re-instituted a state mask mandate which leverages that potential, a factor that had lapsed even as we are going through the second US Delta surge…. [Do] people with confirmed prior Covid need to get vaccinated…. For Omicron there is very little neutralization antibody activity present in people who have had Covid infections from Alpha, Beta or Delta variants…. In Denmark, the displacement of Omicron for Delta as dominant… is expected… this week…. Now let me get to the critical issue…. Where Omicron has been gaining steam, the proportion of hospitalizations is lower than expected, which is great. However, the main reason for this… is not… the immunity wall that has been built in people throughout the 2 years of the pandemic…. Prior Covid or 2 shots… do not provide much defense against Omicron. The 3rd shot helps, but the effectiveness is considerably lower than what we have seen with Delta…. “It’s the immunity, stupid,” is my simplest, reductionist way to convey the reason for what we’ve seen so far…. We’ll know much more in upcoming days and I’ll try to summarize the ground truths and ideas here…

LINK:

Robert Armstrong & Ethan Wu: The Fed Is Ready. Is the Market?: ‘A week ago, Unhedged stuck its nose above the parapet, and smelled fear. With tighter policy arriving soon, we argued, the market was poised to struggle. The market, naturally, responded to our hubris by ripping higher…. Economic growth is just plain very high…. Stagflation this ain’t, not even nearly…. The 10–2 yield curve suggests that while the Fed will push up short rates, growth will not be strong enough over the long term to push longer rates up. Indeed, ten-year yields are a few basis points lower that they were when Covid hit…. If you are worried about inflation or you see sustained growth ahead, the bond market is absolutely shouting that you are wrong. Here’s the 10–2 curve and 5-year inflation expectations…. What has Unhedged sticking to its gloomy (or at least gloomy-ish) view is the broader context. Higher rates, tighter fiscal policy, high stock valuations, slowing earnings growth, and a slowing Chinese economy are a tricky combination…

LINK: <https://www.ft.com/content/c75fa831-0cc3-498f-976d-4993464bb6b0>

Guillaume Blanc: The Cultural Origins of the Demographic Transition in France: ‘Secularization accounts for the early decline in fertility in eighteenth-century France. The demographic transition… took hold in France first… a century earlier than in any other country…. I comprehensively document the decline in fertility and its timing using a novel crowdsourced genealogical dataset. Then, I document an important process of secularization at the time…. I show a strong association between secularization and the timing of the transition. Finally, I leverage the genealogies to account for unobserved pre-existing, geographic, and institutional differences by studying individuals before and after the onset of the transition and exploiting the choices of second-generation migrants…

LINK: <https://www.guillaumeblanc.com/files/theme/Blanc_JMP2.pdf>

Robert Reich: Biden’s Last Stand: ‘Senator Joe Manchin… refuses to vote on Biden’s sweeping “Build Back Better” climate and social spending package before Christmas…. What’s Manchin’s reason? I once thought he was trying to protect West Virginia’s coal mining industry…. But West Virginia’s coal industry employs only around 13,000 workers—less than 2 percent of the state’s work force…. West Virginia’s biggest industry by far is health care, which employs more than 100,000 people (including many middle-class jobs). Build Back Better would make it easier for many West Virginians to get health care…. In recent weeks Manchin has added another twist to his opposition to Build Back Better, raising concerns that it will worsen inflation…. Manchin is riding a wave of negativity about the economy (and is contributing to it with all his worrying statements about inflation)…. Yet apart from inflation, the U.S. economy hasn’t performed this well in years…. Joe Manchin illustrates that the real division in American politics is no longer left versus right, conservative versus liberal, even Democrat versus Republican. The real division is democracy versus the moneyed interests…

Timothy B. Lee: Why Battery Costs Have Plunged 89 Percent Since 2010: ‘The need for predictability is one reason that open-ended renewable energy subsidies are valuable…. Tesla benefitted a lot from the $7,500 tax credit the federal government gives to customers of the first 200,000 battery electric cars a company makes. The credit expanded the potential market for Tesla vehicles, making it easier for Tesla to raise money and to sign long-term contacts with suppliers. Crucially, Tesla knew years in advance that its customers would be eligible…. There’s still room for governments to do more of this…. Iit’s much cheaper for the world to decarbonize together than for any single country to do it alone. And doing it quickly might prove surprisingly affordable…

LINK: <https://fullstackeconomics.com/untitled-2/>

Jay Daigle: Pascal’s Wager, Medicine, & the Limits of Formal Reasoning: ‘A back-of-the-envelope cost-benefit analysis tells us that taking ivermectin for covid might have positive expected value. If we follow that logic to its conclusion, we wind up taking twenty different supplements and this seems like it can’t be wise. A blinkered view of rationality tells us to ignore our intuition and follow the math. A more expansive view realizes that if the numbers we’re plugging into our cost-benefit analysis are shakier than that intuition, then we should take the intuition seriously. Cost-benefit analyses and other “mathematically rational” are only as good as the numbers and arguments that we bring to them. But even with shaky numbers, we can learn things from comparing our intuitions with the result of our calculations…

LINK: <https://jaydaigle.net/blog/pascalian-medicine/>

Re: ivermectin, any positive results of taking ivermectin could easily be from the placebo effect.

> Thus I am markedly less optimistic than is Diane, not about economics—the state of economics, at least where I sit here in Berkeley, is very, very good.

Y'all can't seem to come to grips with food security as an issue. We're getting pretty close to the decade agriculture fails enough that people die in large numbers. This isn't being priced in, which in turn implies the models only see money and not the world.