DeLongTODAY: What Comes After HI—Herd Immunity—Day for þe Economy? 2021-01-15 Fr

My DeLongTODAY Briefing for 2021-01-15 Fr

DeLongTODAY: <http://delongtoday.com>

Google Drive Video: <https://drive.google.com/file/d/1dA87RowGbAH8NMz-IGX0nuUZaZdgcO5Y/view?usp=sharing>

<https://www.icloud.com/keynote/0q8g1NeEGkcO1siJ5uFPDi0Tw>

What Comes After HI—Herd Immunity—Day for the Economy?

DeLongTODAY: 2021-01-14

I am Brad DeLong, an economics professor at the University of California at Berkeley and a sometime Deputy Assistant Secretary of the U.S. Treasury. This is the weekly DeLongToday briefing. Here I hold forth here on the Leigh Bureau’s vimeo platform on my guesses as to what I think you most need to know about what our economy is doing to us right now.

I promised Wes Neff when he agreed to provide the infrastructure for this that I and my briefings would be: lively, interesting, curious, thoughtful, and relatively brief. Relatively.

I promised I would provide briefings on a mix of: forecasting, politics, macroeconomic analysis, history, and political economy.

Today is mostly a macroeconomic situation briefing. Today I play the role of Captain Obvious. I am not going to say anything that I do not regard as totally obvious here…

But first...

====

Right now we are at 400,000 coronavirus deaths. Right now we have 130,000 people hospitalized. Right now we have 220,000 daily cases a day confirmed, and between 350,000 and 600,000 true cases per day.

I confess I do not understand the pattern of this third wave of the coronavirus plague.

If we could push the virus’s reproduction rate R down from the 3 or more it was in the early spring to below one, as we did in April, we ought to have been able to keep it below one. And so we should now look like Japan, or Australia.

But it was only when nationwide hospitalizations were above 50,000 that people became scared enough to change their behavior enough to actually do enough social distancing to put the virus on a downward trajectory. And then, when, hospitalizations got down to 30,000, people relaxed, and relaxed too much, and the virus began to spread again.

This behavior pattern really does not make a great deal of sense to me. If you figure that everyone knows 100 people well, and each of them knows another 100 people well, then it looks as though people become scared enough to take effective action when the typical person heard more than once from their close contacts that one of them in turn had a close contact in the hospital with COVID. But then why slack off and shift state, back to not worrying enough, when that number drops even a bit below 1?

And why did the factors that lead to fear-generating stay-at-home and social-distancing behavior in the spring and summer not operate this winter? Is it that in winter, many more of us withdraw into built environments that are too much like batcaves? But setting up big fan and getting them going is easy, cheap, and reasonably effective. Why are not people altering their indoor environment?

Plus there is another scary thing: We are not yet sure that we have seen the effects of Christmas on coronavirus spread.

====

Let us take a step back and look at the broad picture of the plague as a whole.

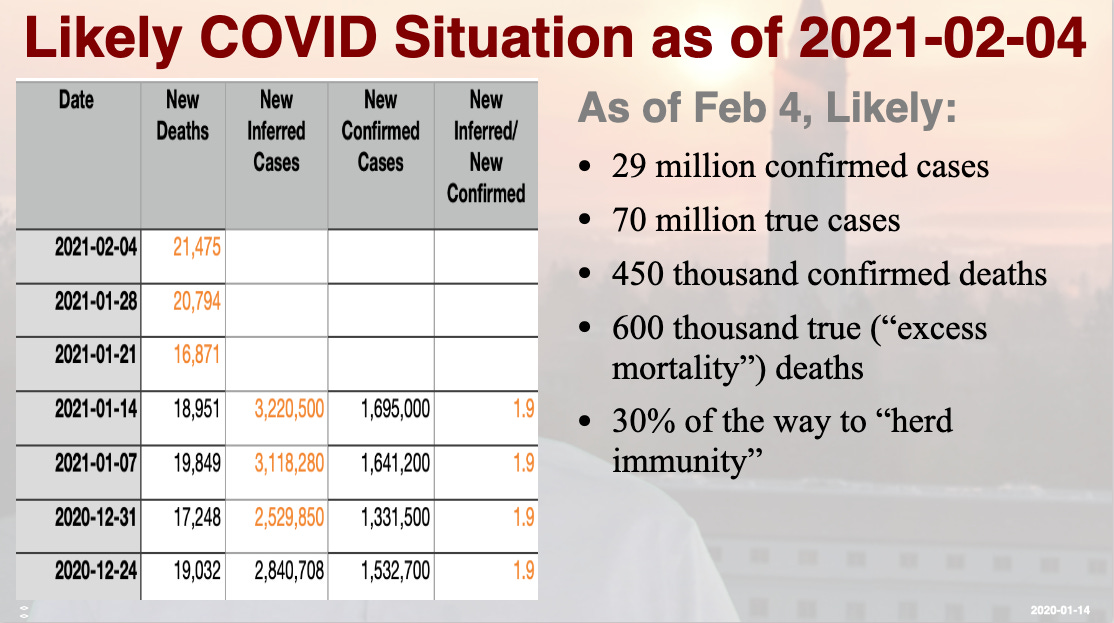

It looks like, as of February 4, we are likely to have hd about 29 million confirmed cases. That, perhaps, means something like 70 million true cases. That then puts us perhaps 25% of the way to herd immunity from cases alone, if significant infection manages to give you two years or more of effective resistance. Also, as of February 4, we are likely to have had 450,000 confirmed deaths from coronavirus. However, we really should take the “excess mortality” metric, The death toll from coronavirus by that metric will, by February 4, be something like 600,000 in total. Many of those in the difference are direct coronavirus deaths that were not properly recorded. Some of those in the difference are people who died because they could not get the treatment they would have gotten in a normal year.

Now there are those who point out, over and over and over again, that the bulk of deaths are coming from people above 75. And then then they go on to say that it should require 10 deaths of people over 75 to make us as disturbed as, say, one death of a 20-year-old who would otherwise be likely to live to 90. Over 75s are not losing that many years of life. Those years of life are achy. Thus, they say, it is false to claim that we are suffering the equivalent of a 911 In every day. Rather, they say, we are only suffering the equivalent of a 911 or two every week.

To which my reply is: what is your point? That it is not as huge a disaster for society as if we were losing 3000 20-year-olds dead each day in a stupid and avoidable military or public health catastrophe does not mean that it is not a stupid and avoidable public health catastrophe. A that does not mean that the human mortality and morbidity losses do not outstrip the narrowly economic losses in wealth and porduction by a full order of magnitude.

====

Thus, as I see it, President-Elect Biden and his team could lead us down three possible roads after inauguration day.

First, they could call for another two week lockdown. If observed nationwide, cases then go back down from 600,000 to 100,000 a day after two weeks, and from 3000 to 500 deaths a day. Thereafter, cases would slowly rise from community transmittion. And mass vaccination kicked in. We would wind up in four months or so with an additional 60,000 deaths, direct and indirect, from coronavirus. Then the plague would be over. And the disease would have done 33% of the work, while the vaccine would have done 67% of the work, to get us to herd immunity.

Or Biden could continue with exhortations for social distancing at their current level and effectiveness. He could rely on a massive vaccine rollout as his principal coronavirus policy. In that case, true cases are likely to rise to 1 million a day. That is 5000 deaths a day. In that case ,we will wind up with an additional 600,000 deaths: a total of 1.1 million or more. And in that case, the disease would wind up doing 75% of the work and the vaccine only 25% of the work in getting us to herd immunity. In that case, we will turn out to have have wasted much of the effort and energy of our biologists and biotechnicians in rapidly building the vaccine. In that case, we will then look at a New Zealand or Australia or a Taiwan or a Korea or Japan, or even a China, in which the vaccine does essentially 100% of the work. And we will feel like the failures that we are.

Or Biden could call for another lockdown, and half of the states and their governors would ignore him. In that case we wind up halfway in between.

Put me down, strongly, on the side of another lockdown.

First, it would it be worthwhile in avoiding 550,000 deaths.

Second, there are also the tail scenarios that I have not yet spoken about. Perhaps the newer, faster spreading versions of the virus mean that if we do not get ahead of it with a lockdown, the vaccine rollout will be too late. It will wind up having had essentially no impact on the death toll. Perhaps we are than talking about health system collapse, and 1 1/2 million total deaths if we stay the course.

Or maybe Biden’s team can think of something really clever.

But, starting from where we are now, clever things are overrated. Clever things will not work because the virus is so widespread. Clever things are all about the dance, and the dance is only for a country that has a relatively low virus prevalence. Starting from now, we need, once again, the hammer.

That, at least, is my view.

I am aware that I am well outside of my wheelhouse here. But I am, once again, not getting good guidance from those who are not to be in the wheelhouse. And I think that I am likely enough to be correct that this is an important thing to say.

====

One of the national treasures brought to minor prominence during the pioneering days of the Internet was Bill McBride of http://calculatedrisk.com. He did much much more than any 100 typical mainstream academic and policy finance and macroeconomists to try to guide us onto a better path during the Great Recession of 2007 to 2010. And I am not even counting the Famas and the Cochranes and the Lucases who actively tried to guide us onto a worse path.

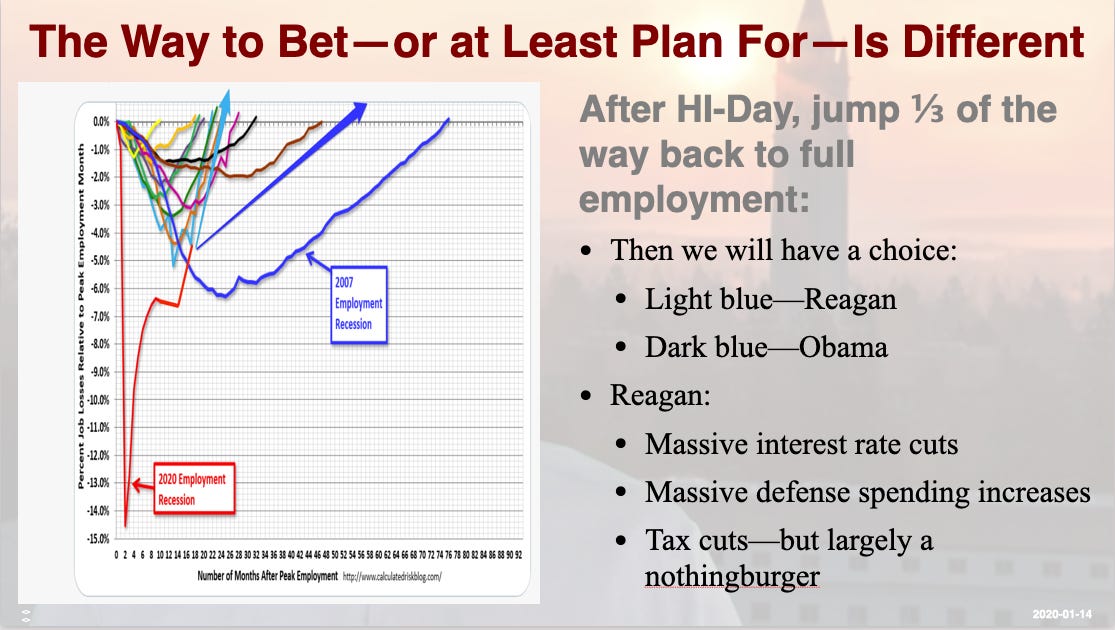

Bill McBride now has an updated version of his “scariest jobs chart ever”—the chart comparing the employment impact of the coronavirus recession to that of previous recessions and depressions since World War II.

The initial downturn from the shutdown and panic shock of the spring of 2020 was more than twice as great as the Great Recession of 2070-2010. Since then we have bounced back halfway. But now the recovery has stalled.

The recovery has stalled because people are still scared enough that whole bunches of employment, employment that is going to come back, are unlikely to even be possible to think about until the virus is widely disseminated and HI-Day—Herd Immunity Day—is here. That will take another four months.

What that means is that, as far as the recovery is concerned, we are going to be marking time until June. After that, recovery can resume.

Until June, what we need is income support targeted to the people whose economic positions have crashed as a result of the coronavirus plague. $2000 checks are an inefficient policy to deliver such income support. But ithey are a policy that might will attract 10 Republican votes in the Senate, and so pass. I know of no better policy that would attract, even possibly, 10 Republican votes in the Senate.

And until those whimpering about how $2000 checks are a bad idea come up with a better alternative that is immediately politically feasible to provide the needed income support to those whose economic positions have crashed, I am going to ignore them. I am going to tell them that they are not being useful. Yes I am looking at you, friend and teacher Olivier Blanchard. Yes I am looking at you, friend and teacher Larry Summers.

ThereI is also the question of extra support for small business entrepreneurs. Small business. I hear often these days from the center-left, is not important. I hear people saying: “one restaurant shust down permanently; somebody else starts up a restaurant in the same space; no biggie. And even if you go from Six restaurants down to four in a townn as a result of all this, that should not be an item of substantial public concern.”

I disagree. The purpose of the government is to provide social insurance. That means that when people get totally shafted by things that are none of their own fault, they deserve support—unless, perhaps, you can accurately claim that the shafting has some powerful ancillary benefit in terms of incentivizing an even more productive reallocation of economic activity toward high value sectors.

This is a proper object of public concern.

People willing and able to start and then run businesses, even the smallest businesses, are very useful people to have around. And, in the normal course of things, the rest of us exploit small-business owers: most of them work very hard indeed, and most of them do so for incomes that are not that large. Treating them like dogs when, because of coronavirus, out of no fault of their own, their business have crated. Well, that will make them rightly think that it is not their government that is ruling in the country. And God knows we do not right now need any more energetic and active people believing, correctly, the government does not work for them.

Besides: it is a mean thing to do..

There are many and important decisions to be made about how to provide income support over the next four months. There are many and important decisions to be made about how, given the existing political constraints on action, to get a near-term income-support program passed and implemented. My advice to all of you as to how you can help here is to have the back of Biden and his team: they are in the hot seat, and they need support; they do not backseat driving and whingeing right now.

====

Then, in the not quite immediate term, we have the problem of true recovery.

Figure June 1 for Herd Immunity Day, if we are lucky. Then employment will still be 6.5% below its previous peak. Then things still will be worse than at the nadir of the Great Recession. In the Great Recession the employment peak came in January 2008 and the trough came 25 months later, in February 2010. The Obama response that had been designed in December 2008 was clearly inadequate by March 2009. Yet there was no second wave of support. And, in fact, Obama abandoned any chance of further effective effort at cushioning the downturn and speeding recovery in January 2010, when he and a bunch of real geniuses in the White House decided what they really wanted to do was get at the head of austerity parade. So he used his State of the Union address to call for a spending freeze—and threaten to veto any proposals and then—Democratic congress might pass that year that were not sufficiently austere.

I have been looking for a decade for who was responsible for this.

I have not found anyone, save for OMB director Peter Orszag, willing to take any blame. Orszag has long said that he made a big mistake in judging the macroeconomic situation. Kudos to Peter. Trust him. People who at the time did not make it very clear that they were strongly opposed, and have not been public about what happened and why since? Not so trustworthy.

I have heard rrom a number of low-level staffers that the way the Obama White House understood the world was that they won political and media victories by winning the approval of David Brooks. Thus any policies that would interfere with the wooing of David Brooks were non-starts.

I have heard from a number of low level staffers that the Treasury was simply missing in action: That Tim Geithner did not believe that fiscal policy was effective, did not believe that monetary policy was effective, did believe that the only thing that was effective was restoring business confidence, which could not be done by any means other than guaranteeing high profits to bankers and executives and letting any bygones be bygones. But these people may not be viewing the Geithner Treasury objectively. I really do not know

I also do not know the extent to which and Obama administration pushing very hard for a more rapid recovery would have had an effect. Would it have been completely blocked in the Congress by Republicans and blue dogs with respect to fiscal policy? Would it have been blocked with respect to monetary policy by the combination of a Ben Bernanke unwilling to move to do the right thing without a consensus on the FOMC, and a bunch of Republican-appointee Federal Reserve Bank presidents who were totally unwilling to mark their beliefs to market and so recognize what the right thing was? Im any event, it was not tried. There were no new policy initiatives to cushion the depression and significantly speed recovery after March 2009. Thus the dark blue line. And the disaster of the anemic Obama recovery.

====

This time, we hope to avoid the extra near-year of dithering that made the Great Recession trough February 2010 rather than May 2009. And we also hope to avoid the fact that, because the government did not have its foot on the gas, the piece of recovery was appallingly, distressingly, criminally slow after February 2010.

Now there are many right now to point out that, perhaps, this time, the government should keep its foot off the gas.

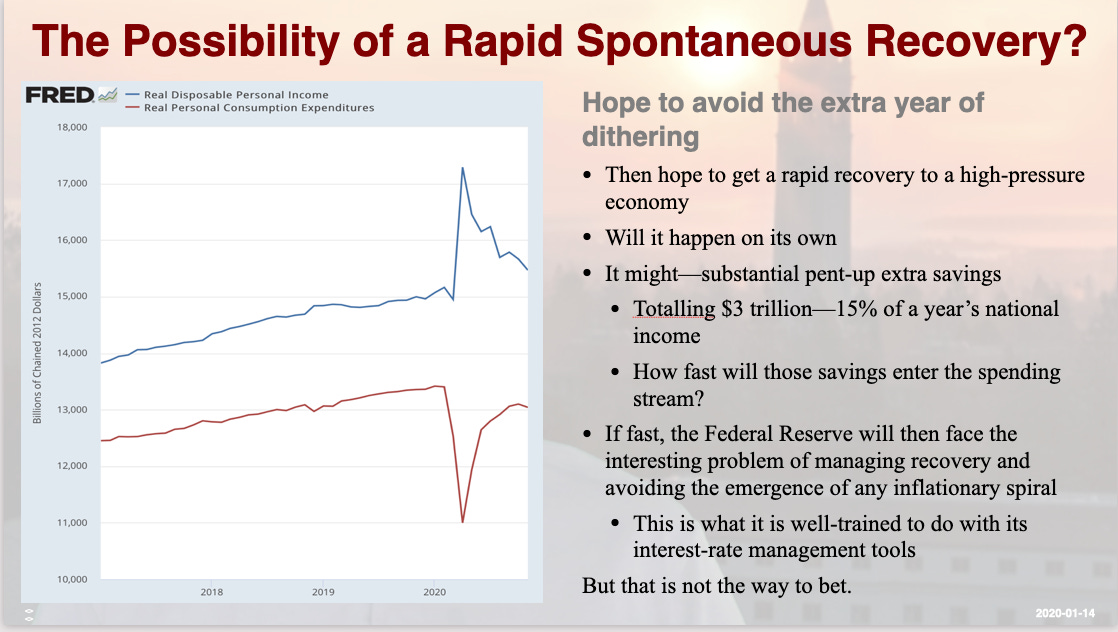

They forecast that a rapid recovery will happen on its own.

And, indeed, it might. There are, after all, very substantial pent-up extra savings in people’s pockets. They might be spent rapidly in a giant Mardi Gras, once HI-Day arrives. Such a giant Mardi Gras could rapidly carry the economy back to full employment. The extra savings American households have accumulated since the plague struck now total more than $3 trillion. That is 15% of a year’s national income.

If People were to spend a third of those, that would be a five percentage point boost to economic growth in the year or so of rapid recovery post June 2021. In that case, the Federal Reserve would then face the conceptually interesting problem of managing recovery and avoiding the emergence of any inflationary spiral. Dealing with this kind of problem is what the Federal Reserve is well trained to do, and what its interest rate management tools are for.

I think that, if that optimistic scenario develops, we can leave the task of proper stabilization policy and macroeconomic management to the Federal Reserve

But that is just one of the possible scenarios.

If we get a more pessimistic outcome, the Federal Reserve cannot help us. So the rational thing to do is to plan for the worst, and not only to plan for the worst but to start right now implementing plans to deal with the worst. If the optimistic scenario comes true, those plans can be cut short. The federal reserve will have the baton and knows how to run that particular race. If not, we will really wish then that we had started dealing with the situation right now, in what will be our future selves’ past.

====

So what outcome do we want to plan? The outcome we want to plan for sees, soon after HI—Herd Immunity—Day, the economy will jump 1/3 of the way back to full employment. That will then leave us about as far below the previous employment peak as the US economy was in 1982, at the depth of the Reagan recession. Curiously and by chance, the time between the last employment peak and the trough of the Reagan recession was about as long as the time between the last employment peak and June 2021. The path employment took to get there, however, was very very different indeed.

After the end of the Reagan recession, the Volker deflation, there came the Reagan boom.

They were seven very fat years for the upper class.

They were seven better years for most of the country.

They were a disaster for midwestern manufacturing: The beginning of the transformation of America’s world class industrial built into the rustbelt, largely, I think, because both George Shultz and James Baker were too dumb to listen to Marty Feldstein—but that is a fight that I think the good guys lost almost 2 generations ago. The Midwest aside, for most of the country the Reagan recovery was all anyone could ever wish. A striking contrast with the Obama recovery.

So how do we get the Reagan recovery? We got it because Paul Volker at the Federal Reserve responded with rapid and enormous interest rate cuts. We got it because Reagan’s wanting to heat up the Cold war produced massive defense spending increases—which in the end did nothing at all for America’s national security, as the new military was built up to confront an adversary that was at that moment ceasing to exist. And then there were the Reagan tax cuts, which were as close to a complete nothingburger as far as boosting investment and even boosting production and employment were concerned as, well, the Ryan-McConnell-Trump tax cut was. Did nothing except transfer wealth upward and make America a more unequal and very visibly less-fair place

We cannot cut interest rates. So we will have to rely on expansionary fiscal policy: the federal government buying useful things and putting people to work doing useful things, pus providing aid to states to keep them from turning into little Herbert Hoovers again. That is what we need to get the economy on the light blue recovery track rather than the dark blue recovery track.

====

There will, of course be the devotees of austerity.

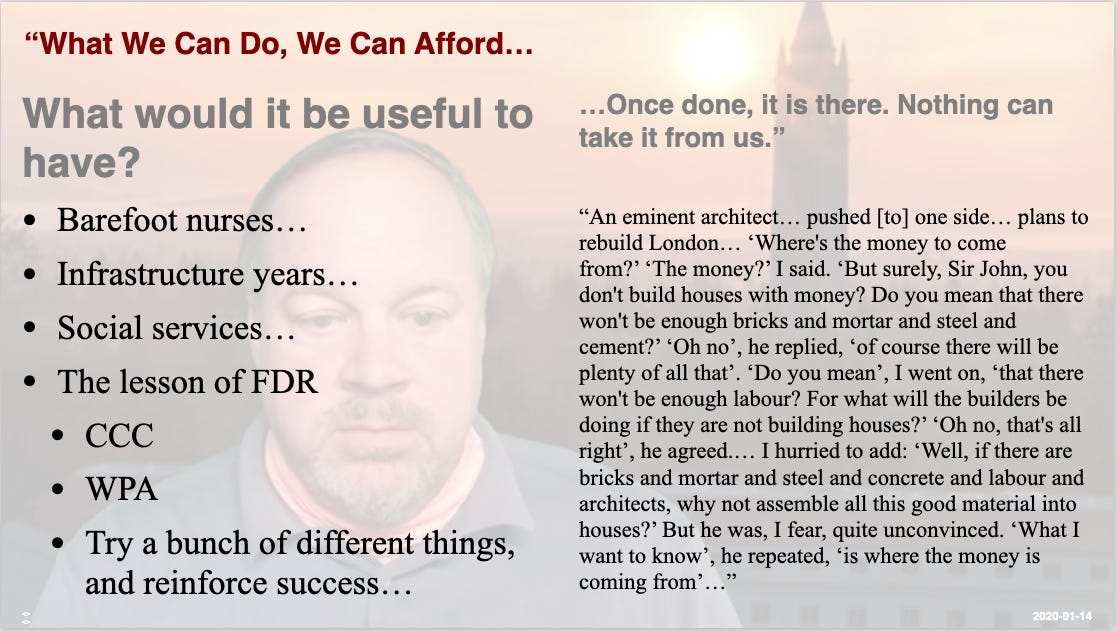

The answer to their arguments, of course, is the same as the answer was back in 2010—the answer that the Obama administration did not then give. It is the answer given by John Maynard Keynes during World War II. As long as there are unemployed people who want to work, society can do more. We can afford it. Whatever we can do, we can afford. Yes, there are problems with arranging the financial scaffolding so that the financial scaffolding supports the actual work being done and is sustainable. But we are clever enough to solve those problems. They are not very hard.

Keynes spoke to a BBC radio audience during World War II about his attempt to argue with those who said that Britain could not afford to rebuild London to repair the damage from the Nazi bombings because “where would the money come from”:

“An eminent architect… pushed [to] one side… plans to rebuild London… ‘Where's the money to come from?’ ‘The money?’ I said. ‘But surely, Sir John, you don't build houses with money? Do you mean that there won't be enough bricks and mortar and steel and cement?’ ‘Oh no’, he replied, ‘of course there will be plenty of all that’. ‘Do you mean’, I went on, ‘that there won't be enough labour? For what will the builders be doing if they are not building houses?’ ‘Oh no, that's all right’, he agreed.… I hurried to add: ‘Well, if there are bricks and mortar and steel and concrete and labour and architects, why not assemble all this good material into houses?’ But he was, I fear, quite unconvinced. ‘What I want to know’, he repeated, ‘is where the money is coming from’…”

====

So the right answer is: what would it be useful to have?

That is what the government should spend money on.

We need to have a lot of barefoot nurses, both to fight coronavirus and to fill in the appalling holes in America‘s health system, by which we spend 50% more money then any other country and yet are significantly sicker, with a five year or more gap in life expectancy vis-à-vis countries that do it right.

We should have infrastructure week. May, we should have infrastructure years.

We should have social services. A Substantial part of the unrest of 2020 came from the fact that we have been sending our police to do jobs that they are not well trained to do. If you look around at what happens on the streets and in the houses of America, you easily convince yourselves that we want many many social workers then we have.

The basic lesson is that of FDR. We want to put people to work doing useful thanks. A Civilian Conservation Corps might be nice. A Works Progress Administration might be nice. Roosevelt’s genius was that he was willing to try a bunch of different things, and then willing to reinforce success and ruthlessly cull failure. That is the proper way for getting the country back to full employment, and getting the country full employment quickly, once HI-Day is upon us.

So I urge all of you: Go out there and talk to people, and make this project politically feasible.

I’m Brad DeLong. This is my DeLong Today briefing.

4002 words