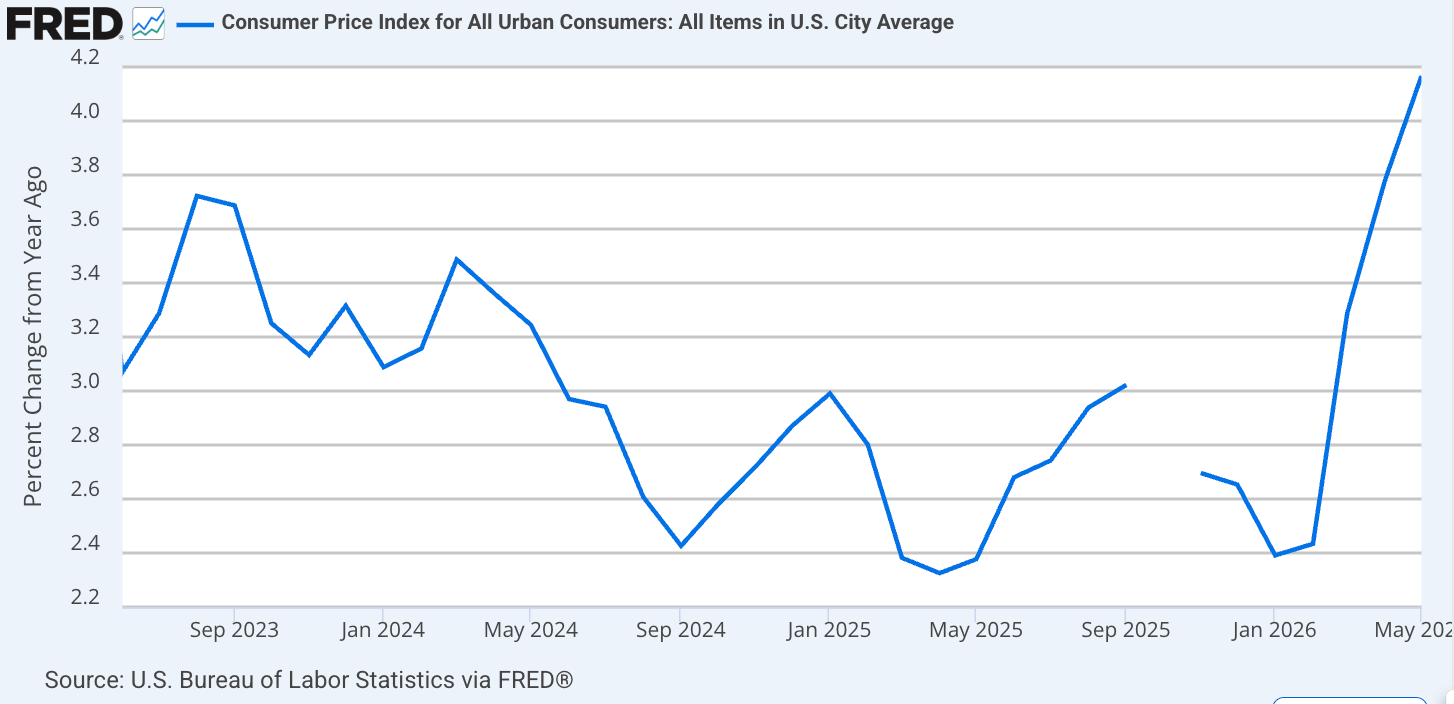

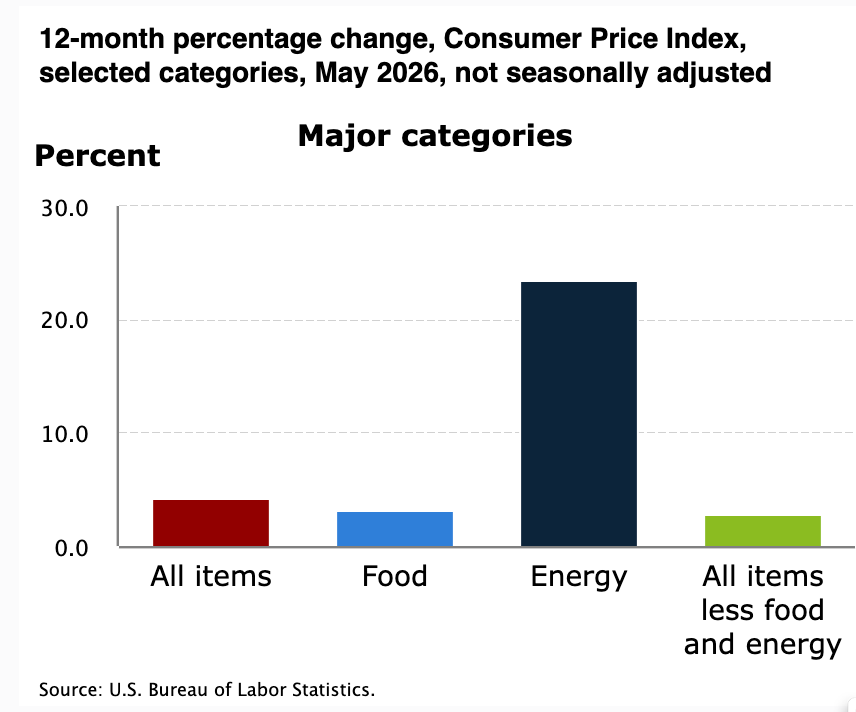

So Far Inflation's Return Limited to Energy. So Far: CHART OF THE DAY

Monetary policy risk returns as new Fed Chair Kevin Warsh begins cosplaying Arthur Burns in the 1970s. Inflation is back. The oil shocks are too. The lying never left. The price level jumps, new...

Monetary policy risk returns as new Fed Chair Kevin Warsh begins cosplaying Arthur Burns in the 1970s. Inflation is back. The oil shocks are too. The lying never left. The price level jumps, new Fed Chair Kevin Warsh wobbles, Trump and the Trumpists cry “Cut interest rates!”, and Kevin Warsh has promised them that he would…

Yes: he is here: at the table in the center of the room where the FOMC meets: Lord Banquo, Thane of Lochaber:

2022’s inflation is coming back to us again:

The BLS reports:

BLS: <https://www.bls.gov/>: ‘CPI for all items rises 0.5% in May; gasoline and shelter up: In May, the Consumer Price Index for All Urban Consumers rose 0.5 percent, seasonally adjusted, and rose 4.2 percent over the last 12 months, not seasonally adjusted. The index for all items less food and energy increased 0.2 percent in May (SA); up 2.9 percent over the year (NSA)…

Scott Bessent falsely claims that this return of inflation will be followed by deflation:

Scott Bessent: <https://www.ft.com/content/b8d9c334-f7c5-4806-b2db-75dda9ae6613?syn-25a6b1a6=1>: ‘Except for inflation, which is, I believe, going to be a short-term blip, the economic data is very strong…. I think we have all the makings for a very strong economy. I think that we have temporary elevated prices that will come back down…

I could say that he has clearly been drinking too much from the Straits of Vermouth, but actually he is just a bald-faced liar: he does not think “elevated prices… will come back down”. The price level is undergoing another oil shock-driven jump-up, and the question is whether medium-term inflation expectations remain anchored or not. And the answer to the question is something we do not know.

Meanwhile, in the center ring of the circus, Kevin Warsh told a lot of lies to somebody in the process of his getting to be Fed Chair. But we do not know who he was lying to. Was he lying to Trump when he told Trump he would not raise rates and would cut rates whenever he could get the committee to vote for it? Or was he lying to all those he told sotto voce that he would be a “normal” Fed Chair rather than a corrupt Trumpist hack? We may learn something about this at the FOMC meeting next week.

Recall that Trump has demanded things of Warsh:

Myles McCormick: Donald Trump piles pressure on Kevin Warsh with call for rate cut <https://www.ft.com/content/056789c0-d316-4b02-be24-2f75208790dd?syn-25a6b1a6=1>: ‘Donald Trump has piled pressure on Kevin Warsh ahead of his first meeting as chair of the Federal Reserve by demanding lower interest rates…. “There’s no reason to raise interest rates,” Trump told NBC’s Meet the Press. “We built the country by doing great and having rates low. What they do is when they raise interest rates, they try and kill success. I don’t want to kill success. We should actually lower interest rates.”… Trump has called for the Fed’s benchmark rate — currently in a range of 3.5 to 3.75 per cent — to be slashed to 1 per cent or lower…. “We’re doing great, and it’s unfair that whenever you do great, they want to raise interest rates,” said Trump. “It should be the opposite way.”…

“Kevin is fantastic, and I want him to do whatever he wants. I don’t want to have a big influence on him,” Trump told NBC. “But my feeling is that when a country is doing well, they shouldn’t be penalised by immediately raising interest rates. They should actually be incentivised”…

For all of us born in 1960 or before, the memory of Arthur Burns’ tenure as chair of the Federal Reserve—and then G. William Miller’s hapless attempts to thread the needle before he was moved over to the Treasury and Volcker brought down the hammer that produced the depression of 1982—is Banquo’s Ghost at the feast. If history regularly repeated itself, we would be living through another supply shock, followed by a period of accommodative policy, which led to unanchored expectations, which eventually necessitated a brutal, Paul Volcker-style crushing of the economy to restore credibility. But history is not a prefixed script that is merely waiting for its actors to arrive on stage. We make choices. We make our own history.

The deanchoring of inflation expectations in the 1970s and then the Volcker Moment of 1982 was a response to a crisis of legitimacy. The Federal Reserve of the 1970s was struggling to find its footing in a new, post-Bretton Woods world. Today, the central banks of the advanced economies possess a level of institutional maturity, autonomy, and toolkit sophistication that would have seemed like science fiction to their 1970s predecessors. They have learned the hard lessons of the past. They are not just watching inflation; they are actively managing the expectations that drive it—or were, until Kevin Warsh became Fed Chair.

And when he takes his seat in the Chair’s chair next week, Banquo’s Ghost will be looking across the table at him.

I like the FT copyright warning inclusion beginning with "Please use sharing tools ...". For some reason, it is hilarious. Are they that desperate not to be quoted? I assume they shoved it in when you did the copy.

As for inflation, time will tell. The current Trump policy is that he doesn't care about inflation, but a lot of people in the US do. We really haven't seen the effects of the fuel price shock yet. This fall they'll be more obvious, and there's a good chance Trump will still be "negotiating" with Iran.

The question is whether the actual infaltion outcomes resulting from Fed policy instruments acticting on the exonomy are enough or too much to faciitate adjustment to the latest supply shock. Today's inflatin news pushes in the "too much" direction, but holding off of an increase in interst rates still seems prudent. TIPS on the other had has been headed down, whic implies to me that a smidgen of tightening woud not be out of place.