THE MACRO-FINANCE SITCH: The Streams (of Falling Short-Term & Rising Long-Term U.S. Treasury Rates) Cross

In this case, the yield curve uninverts—and yet expectations remain for substantial declines in future short rates. How can this be? Arithmetically, by the "term premium" rising. But what does that...

In this case, the yield curve uninverts—and yet expectations remain for substantial declines in future short rates. How can this be? Arithmetically, by the "term premium" rising. But what does that term premium rise mean?

In the words of Egon Spengler of the Ghostbusters Team: “Don’t cross the streams!” Yet since September the streams have crossed—falling short-term and rising long-term U.S. Treasury interest rates bringing what looks to me like a premature uninversion of the yield curve. Is it the bond vigilantes cleaning their weapons in anticipation of having a Liz Truss Party for the arriving Chaos-Monkey-in-Chief? Or is it a very interesting but rather technical market microstructure phenomenon? I have a weak belief it is the second…

Yesterday AM we had the very sharp Torsten Slok raising possibilities, and reminding us of how British Prime Minister Liz Truss and her Chancellor Kwasi Kwarteng triggered the appearance of a “Moron Premium” in British government long-bond yields that immediately cost them their jobs:

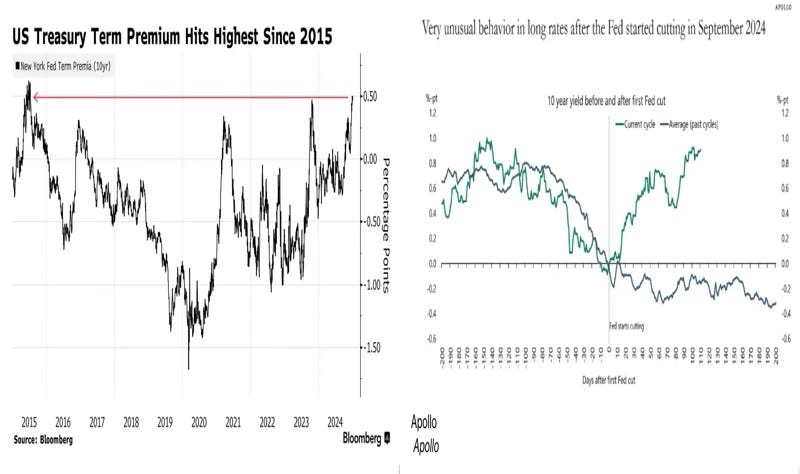

Alice Atkins & Lisa Abramowicz: “Rising [U.S.] Treasury Yields Risk a ‘Truss Moment,’ Apollo’s Slok Says”: ‘Treasury yields have been rising so fast that there’s a risk of bond market turmoil resembling the upheaval that led to the resignation of then British Prime Minister Liz Truss, according to Apollo Global Management’s Torsten Slok….. Concern about how the US will manage its ballooning debt burden, especially at a time that incoming President Donald Trump has promised to deliver tax cuts.… Worries bubbling up that Trump’s policies will fan inflation and unsettle bond investors…. Bond market anxiety… seen in… the term premium… the additional [expected] yield that investors demand to hold long-dated debt instead of [following the strategy of] rolling over shorter-term securities… [which] hit the highest level since 2015…. “80% of the increase in long rates since September has potentially been driven by worries about fiscal policy,” said Slok… <https://www.bloomberg.com/news/articles/2025-01-07/apollo-s-slok-says-rising-treasury-yields-risk-a-truss-moment>

Below (a) the term premium, and (b) a nice plot by Slok of how this easing cycle really is different as far as the reaction of the ten-year Treasury rate is concerned:

The key point: this upward jump in the second half of 2024 is not a belief that short-term interest rates will be higher in the future. It is, rather, a belief that short-term interest rates in the future are very uncertain, and thus that you need to be paid more in order to buy a long-term bond right now and so lose your ability to react when short-term rates change. So what is causing this belief?

This AM Paul Krugman chimes in, with what he says “may be wishful thinking”, making the case that this substantial—0.8%-point—upward move in ten-year interest rates since September is history rhyming—occurring the first time, as farce, and appearing the second time, as farce as well: a Moron Premium as “the bond market [is] starting to suspect that Trump really is [the unleashed chaos monkey] who he seems to be”:

Paul Krugman: “Is There an Insanity Premium on Interest Rates?”: ‘Look at the dynamic…. Jeff Stein… reported… people around Trump were planning a fairly limited, strategic set of tariffs…. Trump quickly responded with a Truth Social post calling the report “Fake News” and declaring that he does too intend to impose high tariffs on everyone and everything. In short, Sources: “Trump isn’t as crazy as he looks.” Trump: “Yes I am!” Then, as if to dispel any lingering suspicions that he might be saner than he appears, Trump held a press conference in which he appeared to call for annexing Canada, possibly invading Greenland, seizing the Panama Canal and renaming the Gulf of Mexico the Gulf of America. This morning CNN reported that Trump is considering declaring a national economic emergency — in a nation with low unemployment and inflation! — to justify a huge rise in tariffs…. But, you may ask, if bond investors are starting to worry about the madness of Trump 2.0, why are stocks up?… [Perhaps] stock… investors are… lizard-brained. Everyone knows about meme stocks…. I haven’t heard of any meme bonds…. [Perhaps]… the recent rise in stocks is… AI…. I don’t want to push this too far…. I don’t want to give in to motivated reasoning…. But rising interest rates even as the Fed cuts may be an early sign of things to come… <https://paulkrugman.substack.com/p/is-there-an-insanity-premium-on-interest>

So what do I think of this?

I think that Paul and Torsten are, more likely than not, engaging in at least a little wishful thinking here.

This feels to me much more like a “market microstructure” phenomenon than a “bond vigilantes cleaning their weapons at the prospect of the reïnstallation of the Chaos-Monkey-in-Chief” phenomenon.

Briefly, it does not look to me like bond traders are thinking that inflationary Trumpist policies will make short-term interest rates higher in the future than we thought they would be back in November. Rather, it looks to me like bond traders have shifted from “we locked in what looked like a very attractive yield” to “we preserved our freedom and avoided exposure to duration risk” as the message they are rehearsing in case they have to explain to their bosses what went wrong. Why they have done this is a fascinating question, but one that would require a deeper dive than I am capable of providing, and one that could not be easily explained by the spread of the “Trump will try to goose inflation” meme.

Much more in the weeds below the fold:

Keep reading with a 7-day free trial

Subscribe to Brad DeLong's Grasping Reality to keep reading this post and get 7 days of free access to the full post archives.