BRIEFLY NOTED: For 2021-06-12 Sa

Things that went whizzing by that I want to remember...

First:

I find this from Mervyn King for Bloomberg annoying.

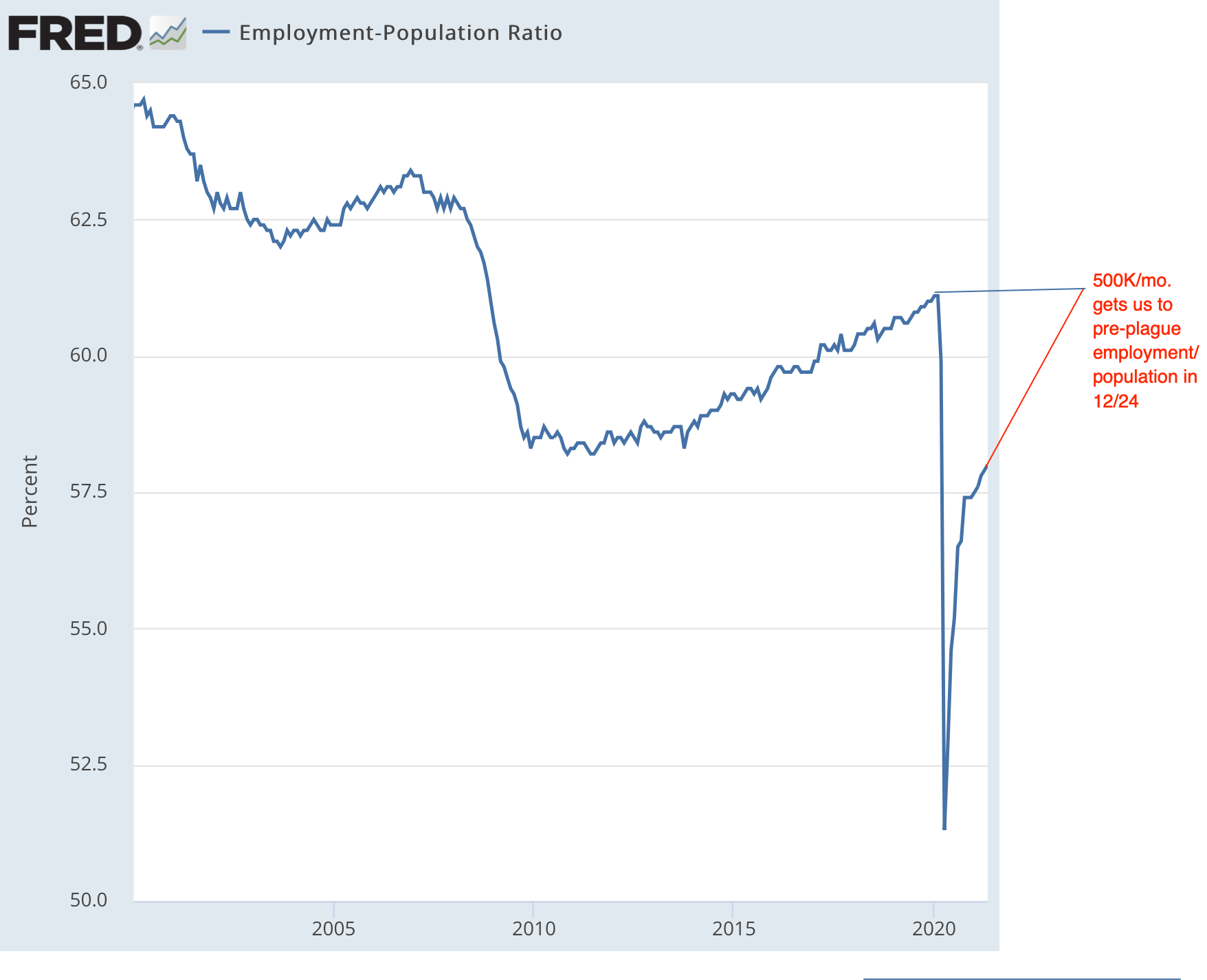

Yes, the risk of inflation is “real”—as it was not in 2008, 2009, 2010, 2011, 2012, 2013, 2014, 2015, 2016, 2017, 2018, and 2019, in all of which we were assured that it was very real indeed. But the risk that the recovery will be anemic is real as well. If inflation risks turn out to materialize, the Federal Reserve has a straightforward way of handling them. If anemic-recovery risks materialize, there is no path to easily handle them. Given the immense uncertainties, an ability to do the math of option value under asymmetric risks mandates that the sensible thing to do is to prioritize rapid recovery now, and to wait until early 2023 to see where we are with respect to inflation.

And, no, we are not “reluctant to criticize the Biden stimulus plans because we share his concerns about [America’s] social and political problems”. We are reluctant to criticize the Biden stimulus plans because they seem sensible ways to (i) provide relief, and (ii) guard against the risk of an anemic recovery like the one that Mervyn King and his peers presided over from 2010–2013. I would be very interested in what Mervyn King would have to say about how to avoid policy mistakes in the future like the ones he played his part in making over 2010–2013. I am much less interested in reading him making false claims about why I and people like me think that insuring against another anemic recovery is job #1 right now, with control over inflation expectations best reserved to be the concern of central banks at some future date:

Mervyn King: Make No Mistake, the Risk of Inflation Is Real: ‘Price stability is when people stop talking about inflation and their decisions reflect genuine economic factors. It has been a long time since inflation was a talking point but, especially in the United States, it has reentered public debate…. Rising input prices and higher output prices reflecting shortages…. Some of these increases may well prove transitory. For the first time since the 1980s, though, two factors make inflation a serious risk: excessive monetary and fiscal stimulus, and weak political resistance…. Many economists are reluctant to criticize the Biden stimulus plans because they share his concerns about the country’s social and political problems. But I’ve seen few challenges to the proposition that the degree of stimulus is out of all proportion to the magnitude of any plausible output gap. And the same logic applies to other advanced economies…. Central-bank independence will be tested over the next few years…. A combination of political pressure to assist in financing budget deficits, promises not to tighten policy too soon, and a growing involvement by central banks in political matters all point to a growing risk that central banks will respond too slowly to higher inflation.

One Video:

John Hennessy and David Patterson: A New Golden Age of Computer Architecture <https://www.youtube.com/watch?v=3LVeEjsn8Ts>

Very Briefly Noted:

Marion Fourcade, Etienne Ollion, & Yann Algan: The Superiority of Economists<https://pubs.aeaweb.org/doi/pdfplus/10.1257/jep.29.1.89>

Jeremy Arnold: First-Principles Journalism: A Blueprinte: ‘What journalism could like look if we rebuilt it from scratch for our times… <https://savingjournalism.substack.com/p/first-principles-journalism-a-blueprint>

Glen Peters: ’How does the global average temperature increase compare to atmospheric CO₂ concentrations in the last ~100 years? It is quite a linear relationship, with a 2.7°C increase for a doubling of CO₂ concentration. This includes non-CO₂ effects, which approximately cancel… <https://twitter. com/Peters_Glen/status/1400776666843058177>

Jeet Heer: Biden’s Democracy Dilemma <https://jeetheer.substack.com/p/bidens-democracy-dilemma>

Matthew Downhour: Applying the Lessons of George’s “Protection or Free Trade”<https://www.liberalcurrents.com/applying-the-lessons-of-georges-protection-or-free-trade/>

Quentin R. Skrabec: George Westinghouse: Gentle Genius <https://books.google.com/books?id=C3GYdiFM41oC&pg=PA230>

Scott Lincicome: The China Threat Meets the China Reality: ‘The view that China is an urgent enough economic threat to justify a broad rejection of free markets is mostly misguided… <https://capitolism.thedispatch.com/p/the-china-threat-meets-the-china>

Wikipedia: Rambler American <https://en.wikipedia.org/wiki/Rambler_American>

Mary Beard (2009): The Roman Triumph<https://www.google.com/books/edition/The_Roman_Triumph/s5rGE5pYG58C?hl=en&gbpv=0>

William Sjostrom: Reviewing: ‘The Box: How the Shipping Container Made the World Smaller and the World Economy Bigger’ <https://eh.net/book_reviews/the-box-how-the-shipping-container-made-the-world-smaller-and-the-world-economy-bigger/>

Schalkenbach Foundation: Protection or Free Trade <https://schalkenbach.org/library/henry-george/protection-or-free-trade/preface-index.html>

Rebecca Pulju: Changing Homes, Changing Lives: Material Conditions, Women’s Demands, & Consumer Society in Post-World War II France <https://quod.lib.umich.edu/cgi/p/pod/dod-idx/changing-homes-changing-lives-material-conditions-womens.pdf?c=wsfh;idno=0642292.0031.018;format=pdf>

Josh Marshall: TPM Inside Briefing With Paul Krugman: ‘Yesterday we held an Inside Briefing with Paul Krugman in which we discussed pretty much all the economic policy questions (and the political debates growing out of them) of the early Biden presidency. We talk about the Biden infrastructure plan, inflation, chronic under-investment, Larry Summers, whether deficits matter and more. If you’re a member, you can watch our discussion after the jump. I think you’ll enjoy it… <https://talkingpointsmemo.com/edblog/tpm-inside-briefing-with-paul-krugman>

Mohamed A. El-Erian: The Return of the Finance Threat?: ‘Given recent history, policymakers would be unwise merely to hope for a best-case scenario in which a strong and quick economic recovery redeems the enormous run-up in debt, leverage, and asset valuations. Instead, they should now act now to moderate the finance sector’s excessive risk-taking…<https://www.project-syndicate.org/commentary/policymakers-must-act-now-to-mitigate-financial-risks-by-mohamed-a-el-erian-2021-06>

Paragraphs:

A very nice rant about how the absence (so far) of (completely definitive) evidence is not evidence of absence, as far as the zoonotic origin of the COVID-19 plague is concerned. Zoonotic origin is definitely the way to bet right now, and those who claim otherwise are bad actors, and are not your friends:

Josh Rosenau: ‘Some have wrongly claimed the natural, zoonotic origin of SARS-CoV–2 is now less likely because it’s been A WHOLE YEAR and we don’t have the wild ancestor. Today, a journal article brings us closer, and shows how hard it’ll be to get the whole story <https://t .co/3iW7mzK2j2>…. 411 bat samples collected in Yunnan province, China between 2019–2020 yields 24 full length coronavirus genomes, including 4 viruses highly related to SARS-CoV–2 and 3 to SARS…. One virus in the sample is now the closest known genetic match to SARS-CoV–2…. Wuhan… is surrounded by areas with significant predicted horseshoe bat diversity…. Finding the exact match will be hard. No wonder it took 14 years for SARS-CoV–1!… Like Ebola and HIV, that intensive field work may not turn up the reservoir and intermediate host(s). Or as with SARS-CoV–1, it could take 14 years…. I hope Nate Silver, Matt Yglesias, Vanity Fair, Wall Street Journal… and other outlets that laundered leaks from Trumpers—repeated their spin that the search can’t pan out and trying to shift blame to China—will give this research just as much airtime. If the origins of COVID matter, this research is far more important than the opinions of: the son of the “fucking stupidest guy on the face of the Earth,” emeritus physicists, MAGA breast cancer doctors, disgraced racist journalists, or Peter Thiel’s manager director.

LINK: <https://twitter. com/JoshRosenau/status/1402826462953017347>

And, right on time, comes evidence about zoonotic coronaviruses closely related to SARS-CoV-2:

Hong Zhou & al.: Identification of Novel Bat Coronaviruses Sheds Light on the Evolutionary Origins of SARS-CoV–2 & Related Viruses: ‘Four novel SARS-CoV–2 related viruses were identified in rhinolophid bats. RpYN06 is the closest relative of SARS-CoV–2 in most of the virus genome. A high diversity of bat coronaviruses was present in a very small geographic area. Ecological modeling reveals a broad range of rhinolophid bats in parts of Asia…

LINK: <https://www.cell.com/cell/fulltext/S0092-8674(21)00709-1>

A very nice interview here about what good anthropologists can bring to economics:

Gillian Tett: Listen to the Silence: ‘How anthropology helps make sense of the world. The FT’s Gillian Tett tells Merryn Somerset Webb why what people aren’t talking about is just as important as what they are, and why combining anthropology with economics can help us make sense of asset prices, markets and the world in a way that pure hard science can’t…

LINK: <https://www.youtube. com/watch?v=uN9YDE5JUbc>

Journal editors hungry for novelty and positive results have definitely put their thumbs on the scale to try to establish that corporate tax cuts boost growth. But they probably do not, at least not by very much:

Sebastian Gechert & Philipp Heimberger: Do Corporate Tax Cuts Boost Economic Growth?: ‘The empirical literature on the impact of corporate taxes on economic growth reaches ambiguous conclusions: corporate tax cuts increase, reduce, or do not significantly affect growth. We apply meta-regression methods to a novel dataset with 441 estimates from 42 primary studies. There is evidence for publication selectivity in favour of reporting growth-enhancing effects of corporate tax cuts. Correcting for this bias, we cannot reject the hypothesis of a zero effect of corporate taxes on growth. Several factors influence reported estimates, including researcher choices concerning the measurement of growth and corporate taxes, and controlling for other budgetary components…

LINK: <https://www.imk-boeckler.de/de/faust-detail.htm?sync_id=HBS-008025>

Feminism and consumer durables in post-WWII France:

Rebecca Pulju: Coming Clean: Another Load of Laundry: ’At the end of World War II, only 37 percent of the buildings in Paris had running water. Remarkably, this figure would have inspired envy in rural France, where only 18 percent of houses had running water. Similarly, a mere 5 percent of France’s homes had a private, indoor bathroom, a luxury to be found in 17 percent of Parisian homes…. Washing clothes required a full day’s labor, as women fetched water from a tap in the courtyard or the street, boiled and scrubbed the clothes, exchanged dirty for clean water, and then rinsed and wrung out their laundry…. It was no surprise, then, that French women’s magazines routinely depicted the pleasures of life in the United States, where domestic appliances appeared to have made housework obsolete…. The image of a home filled with “mechanical servants” was attractive to French women. But having just emerged from years of depression and war and now facing a continuing housing shortage and inflation, most French citizens found the prices of home appliances beyond their reach. Two postwar changes helped to remedy this situation. First, the spread of new spending methods—notably credit—lowered the price of appliances and made them available to more families. Second, French families came to accept that these items, which had been rare before the war, were now indispensable…. French women became extremely creative in finding ways to acquire the machines, even when the price remained high. For one working-class family movement, the solution was washing machine cooperatives…

It remains a puzzle why the army and navy on Oahu and in the Philippines were so ill-prepared for what went down on December 7, 1941. Isn’t this exactly what it was appropriate for the Chief of Naval Operations to do? What else should he have done? Agreed, it would have been nice if he had said something like “an airstrike against Pearl Harbor is a possibility”. But the armament of kido butai gave no clues, and its location was unknown, and the number and equipment of troops and the organization of task forces did suggest an amphibious expedition or expeditions to the south—Philippines, Borneo, & c.:

CNO (1941–11–27): This Dispatch Is to Be Considered a War Warning: ’Negotiations with Japan looking toward stabilization of conditions in the Pacific have ceased and an aggressive move by Japan is expected within the next few days. The number and equipment of Japanese troops and the organization of naval task forces indicates an amphibious expedition against either the Philippines, Thai or Kra Peninsula or possibly Borneo. Execute an appropriate defensive deployment preparatory to carrying out the tasks assigned in WPL 46. Inform district and Army authorities. A similar warning is being sent by War Department. Spenavo inform British. Continental districts Guam, Samoa directed take appropriate measures against sabotage…

LINK: <https://www.ibiblio.org/hyperwar/PTO/EastWind/CNO-411127.html>

(Remember: You can subscribe to this… weblog-like newsletter… here:

There’s a free email list. There’s a paid-subscription list with (at the moment, only a few) extras too.)

With respect to Mervyn King and the concern for inflation, I think you're mistaking the word "inflation" for the technical sense of the term among professional economists. In this context, and I think just about always in a political context, "inflation" means "conditions such that notional wages are increasing". (conditions such that real wages are consistently and generally increasing are generally described as communism, that is, axiomatically intolerable.)

From the viewpoint being presented, the economy exists to increase and perpetuate the relative advantage of the currently rich. If it does anything else, it's not functioning properly and must be corrected. Any notion of general prosperity is something any oligarchy is against.

Re: Mervyn King. Isn't this another case of "not marking one's beliefs to market"? The Wikipedia entry on King suggests to me that the housing bubble and financial collapse has become an idée fixe and subsequent austerity measures are his attempt at redemption to prevent a repeat of bubble formation. IMO, this seems to be the reason for his inflation fears after the injection of so much money to support the economy during the pandemic.